Concept explainers

Videos

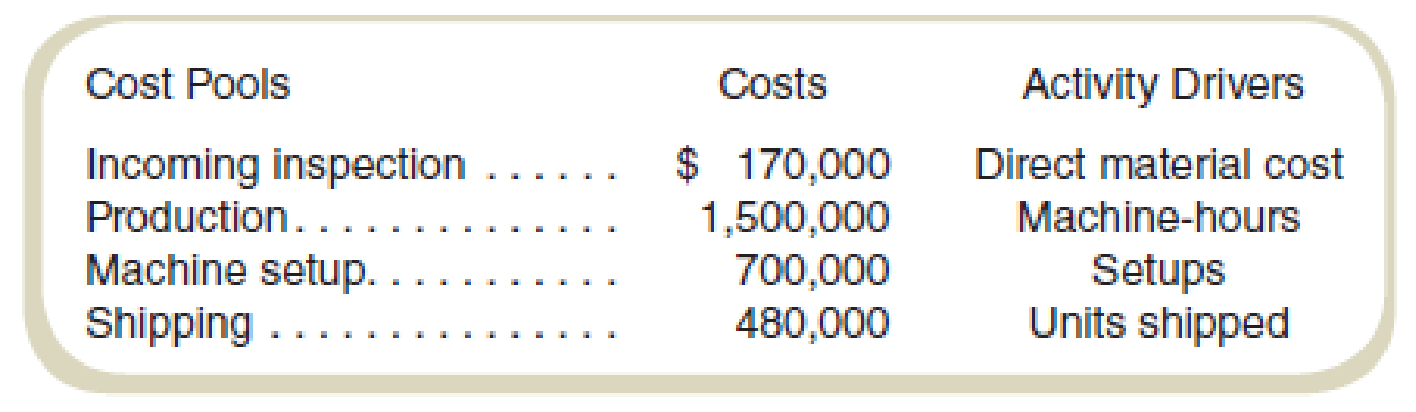

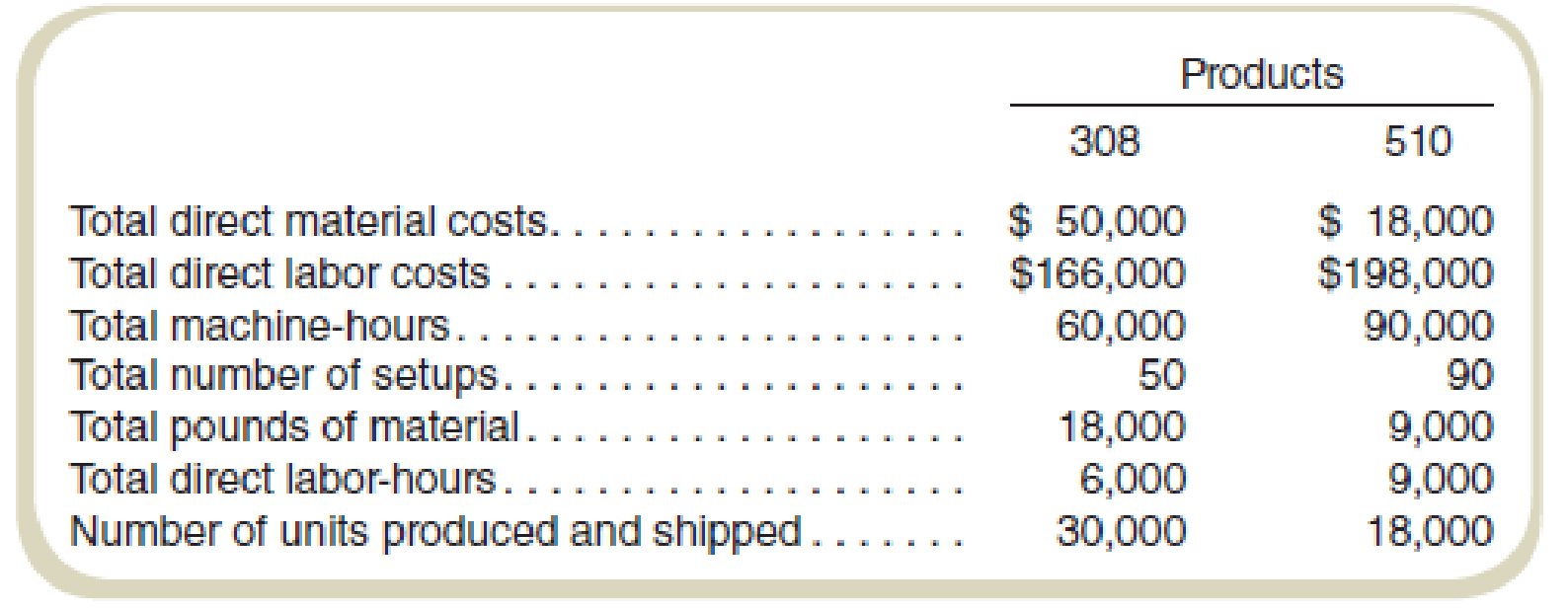

Utica Manufacturing (UM) was recently acquired by MegaMachines, Inc. (MM), and organized as a separate division within the company. Most manufacturing plants at MM use an ABC system, but UM has always used a traditional product costing system. Bob Miller, the plant controller at UM, has decided to experiment with ABC and has asked you to help develop a simple ABC system that would help him decide if it was useful. The controller’s staff has identified costs for the first month in the four

The company manufactures two basic products with model numbers 308 and 510. The following are data for production for the first month as part of MM:

Required

- a. The current cost accounting system charges overhead to products based on machine-hours. What unit product costs will be reported for the two products if the current cost system continues to be used?

- b. A consulting firm has recommended using an activity-based costing system, with the activities based on the cost pools identified by the cost accountant. What are the cost driver rates for the four cost pools identified by the cost accountant?

- c. What unit product costs will be reported for the two products if the ABC system suggested by the cost accountant’s classification of cost pools is used?

- d. If management should decide to implement an activity-based costing system, what benefits should it expect?

Want to see the full answer?

Check out a sample textbook solution

Chapter 9 Solutions

Fundamentals Of Cost Accounting (6th Edition)

- Evans, Inc., has a unit-based costing system. Evanss Miami plant produces 10 different electronic products. The demand for each product is about the same. Although they differ in complexity, each product uses about the same labor time and materials. The plant has used direct labor hours for years to assign overhead to products. To help design engineers understand the assumed cost relationships, the Cost Accounting Department developed the following cost equation. (The equation describes the relationship between total manufacturing costs and direct labor hours; the equation is supported by a coefficient of determination of 60 percent.) Y=5,000,000+30X,whereX=directlaborhours The variable rate of 30 is broken down as follows: Because of competitive pressures, product engineering was given the charge to redesign products to reduce the total cost of manufacturing. Using the above cost relationships, product engineering adopted the strategy of redesigning to reduce direct labor content. As each design was completed, an engineering change order was cut, triggering a series of events such as design approval, vendor selection, bill of materials update, redrawing of schematic, test runs, changes in setup procedures, development of new inspection procedures, and so on. After one year of design changes, the normal volume of direct labor was reduced from 250,000 hours to 200,000 hours, with the same number of products being produced. Although each product differs in its labor content, the redesign efforts reduced the labor content for all products. On average, the labor content per unit of product dropped from 1.25 hours per unit to one hour per unit. Fixed overhead, however, increased from 5,000,000 to 6,600,000 per year. Suppose that a consultant was hired to explain the increase in fixed overhead costs. The consultants study revealed that the 30 per hour rate captured the unit-level variable costs; however, the cost behavior of other activities was quite different. For example, setting up equipment is a step-fixed cost, where each step is 2,000 setup hours, costing 90,000. The study also revealed that the cost of receiving goods is a function of the number of different components. This activity has a variable cost of 2,000 per component type and a fixed cost that follows a step-cost pattern. The step is defined by 20 components with a cost of 50,000 per step. Assume also that the consultant indicated that the design adopted by the engineers increased the demand for setups from 20,000 setup hours to 40,000 setup hours and the number of different components from 100 to 250. The demand for other non-unit-level activities remained unchanged. The consultant also recommended that management take a look at a rejected design for its products. This rejected design increased direct labor content from 250,000 hours to 260,000 hours, decreased the demand for setups from 20,000 hours to 10,000 hours, and decreased the demand for purchasing from 100 component types to 75 component types, while the demand for all other activities remained unchanged. Required: 1. Using normal volume, compute the manufacturing cost per labor hour before the year of design changes. What is the cost per unit of an average product? 2. Using normal volume after the one year of design changes, compute the manufacturing cost per hour. What is the cost per unit of an average product? 3. Before considering the consultants study, what do you think is the most likely explanation for the failure of the design changes to reduce manufacturing costs? Now use the information from the consultants study to explain the increase in the average cost per unit of product. What changes would you suggest to improve Evanss efforts to reduce costs? 4. Explain why the consultant recommended a second look at a rejected design. Provide computational support. What does this tell you about the strategic importance of cost management?arrow_forwardSusan Mills, Company B's chief accountant, has developed an automated costing system that helps track the cost of production activities. This system is capable of accurately measuring and allocating post-manufacturing activities, such as selling, promotional, and distribution activities, in such a way where Company B gets a more detailed view of its product costs. One of the benefits of this system is that it allows Company B to determine which product lines are more profitable. When Susan implemented the new costing system, she realized that the company's current period profits would increase significantly if the new product cost information was used for inventory valuation on the financial statements. Susan has been under intense pressure to improve the company's profits, and this would be a quick and effective way for her to help meet the company's short-term profit goals. As a result, Susan has decided to use the automated costing system to determine the company's profits.…arrow_forwardSusan Mills, Company B's chief accountant, has developed an automated costing system that helps track the cost of production activities. This system is capable of accurately measuring and allocating post-manufacturing activities, such as selling, promotional, and distribution activities, in such a way that Company B gets a more detailed view of its product costs. One of the benefits of this system is that it allows Company B to determine which product lines are more profitable When Susan implemented the new costing system, she realized that the company's current period profits would increase significantly if the new product cost information was used for inventory valuation on the financial statements. Susan has been under intense pressure to improve the company's profits, and this would be a quick and effective way for her to help meet the company's short-term profit goals. As a result, Susan has decided to use the automated costing system to determine the company's profits. 1. Why…arrow_forward

- Southward Company has implemented a JIT flexible manufacturing system. John Richins, controller of the company, has decided to reduce the accounting requirements given the expectation of lower inventories. For one thing, he has decided to treat direct labor cost as a part of overhead and to discontinue the detailed direct labor accounting of the past. The company has created two manufacturing cells, each capable of producing a family of products: the radiator cell and the water pump cell. The output of both cells is sold to a sister division and to customers who use the radiators and water pumps for repair activity. Product-level overhead costs outside the cells are assigned to each cell using appropriate drivers. Facility-level costs are allocated to each cell on the basis of square footage. The budgeted direct labor and overhead costs are as follows: Radiator Cell Water Pump Cell Direct labor costs $168,400 $108,410 Direct overhead 656,760 395,550 Product…arrow_forwardVaughn, Inc produces two types of gas grill: a family model and deluxe model. Vaughn’s controller has decided to use overhead rate based on direct labor costs. The president of the company recently heard of activity based on direct labor costs. The president of the company recently heard of activity- based costing and wants to see hoe the results would differ if this system were used. Two activity cost pools were developed: machine setup. Presented below is information related to the company’s operation: Family model Deluxe Model Direct Labor Cost: $78,000 $156,000 Machine Hours: 2,000 2,000 Setup Hours: 200 800 Total estimated overhead costs are $468,000. Overhead cost allocated to the machining activity cost pool is $280,800 and $187,200 is allocated to the machine setup activity cost pool. Compute the overhead rates using the activity-bases costing approach.arrow_forwardPinnacle Inc. has decided to switch from a traditional overhead allocation system to an ABC system. So far, the firm’s managers have decided that Pinnacle needs six different activity cost pools, including one for assembling products. When selecting a driver for this cost pool, Pinnacle’s managers should be sure to select -the product that appears to account for the majority of the costs in the product assembly pool. - the product that has the highest per-unit assembly cost. - the activity that appears to play the greatest role in determining the firm’s product assembly costs. - the activity that appears to play the greatest role in determining how many units the firm assembles in a given period.arrow_forward

- Bradford Watch Company manufactures luxury and sports watches both for male and female customers. The luxury watches are famous for the high-end design materials while the sports watches are popular for their utilities. The company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding…arrow_forwardBradford Watch Company manufactures luxury and sports watches both for male and female customers. The luxury watches are famous for the high-end design materials while the sports watches are popular for their utilities. The company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding…arrow_forwardBradford Watch Company manufactures luxury and sports watches both for male and female customers. The luxury watches are famous for the high-end design materials while the sports watches are popular for their utilities. The company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: 1. The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding system is fitted with every…arrow_forward

- Pinnacle Inc. has decided to switch from a traditional overhead allocation system to an ABC system. So far, the firm’s managers have decided that Pinnacle needs six different activity cost pools, including one for assembling products. When selecting a driver for this cost pool, Pinnacle’s managers should be sure to select _______ A. the activity that appears to play the greatest role in determining the firm’s product assembly costs. B. the activity that appears to play the greatest role in determining how many units the firm assembles in a given period. C. the product that appears to account for the majority of the costs in the product assembly pool. D. the product that has the highest per-unit assembly cost.arrow_forwardA company manufactures luxury watches made with high-end design materials. The company uses a traditional costing system in assigning overhead costs to the products on the basis of direct labour hours. However, the Production Manager seeks to replace the existing system with the Activity-based Costing (ABC) system to keep control over costs and offer more competitive pricing. After reviewing the existing costing system and interviewing the company’s personnel in relevant departments, the accountant compiled a report highlighting resources and costs involved in manufacturing watches per month: The following table lists out the overhead cost: Activity cost pool Overhead cost (£) Additional Notes Job-order set up 33,000 Procurement and placement 360,000 Installation of winding system 195,000 An auto winding system is fitted with every watch Quality inspection (machine) 60,000 Quality inspection (manual) 21,000 Finishing…arrow_forwardThe Bangor Manufacturing Company makes mechanical toy robots that are typically produced in batches of 250 units. Prior to the current year, the company’s accountants used a standard cost system with a simplified method of assigning manufacturing support (i.e., overhead) costs to products: All such costs were allocated to outputs based on the standard machine hours allowed for output produced. You have recently joined the accounting team and are developing a proposal that the company adopt an ABC system for both product-costing and control purposes. To illustrate the benefit of such a system in terms of the latter, you decide to put together an analysis of batch-related overhead costs. You chose these costs because a previous investigation indicated that there is both a variable component to these costs (materials plus power) plus a fixed component (depreciation and salaries). Last year’s budget indicated that the variable overhead cost per setup hour was $20.00 and that the fixed…arrow_forward

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning

Cornerstones of Cost Management (Cornerstones Ser...AccountingISBN:9781305970663Author:Don R. Hansen, Maryanne M. MowenPublisher:Cengage Learning