Concept explainers

Videos

Entries for

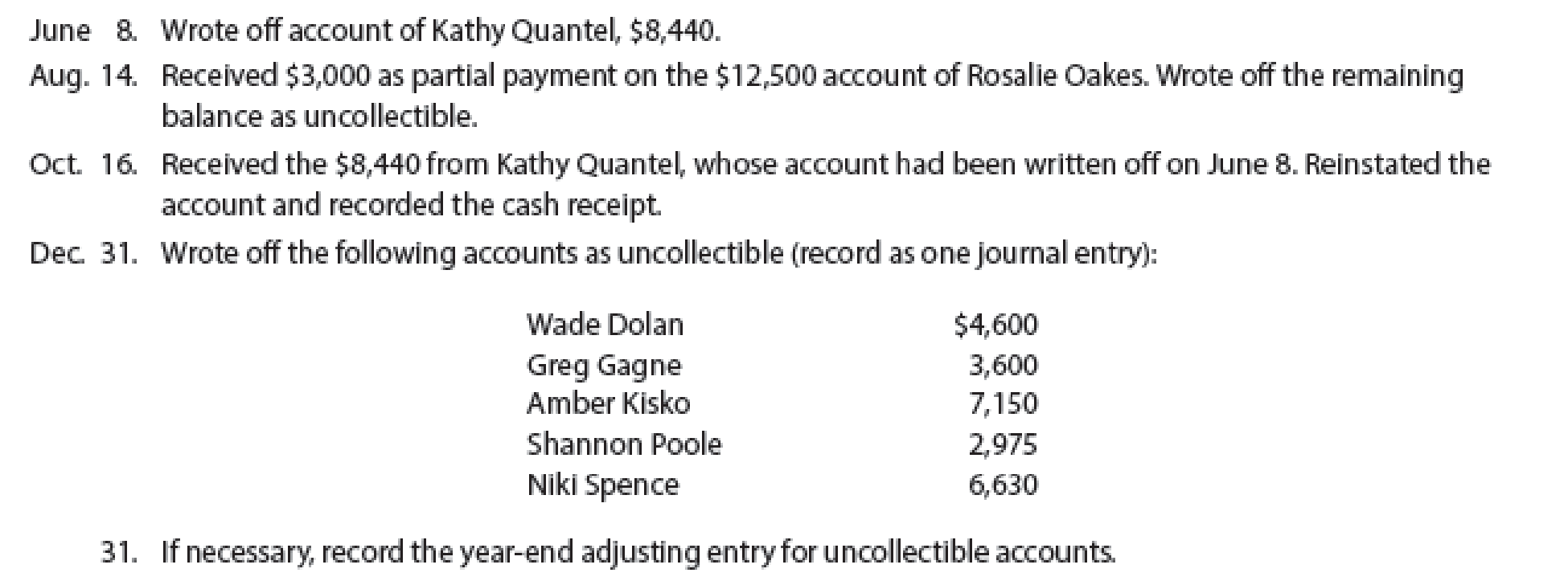

The following selected transactions were taken from the records of Rustic Tables Company for the year ending December 31:

- A. Journalize the transactions under the direct write-off method.

- B. Journalize the transactions under the allowance method, assuming that the allowance account had a beginning balance of $36,000 at the beginning of the year and the company uses the analysis of receivables method. Rustic Tables Company prepared the following aging schedule for its accounts receivable:

- C. How much higher (lower) would Rustic Tables’ net income have been under the direct write-off method than under the allowance method?

A.

Prepare journal entry to record the transactions under direct write off method.

Answer to Problem 14E

Journalize the transactions of Company S under direct write off method.

| Date | Particulars | Debit | Credit |

| June 8 | Bad debt expense | $8,440 | |

| Account receivable – Person KQ | $8,440 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| August 14 | Cash | $3,000 | |

| Bad debt expense | $9,500 | ||

| Account receivable – Person RO | $12,500 | ||

| (To record the cash collection and write-off of remaining uncollectible account receivable ) | |||

| October 16 | Accounts receivable – Person KQ | $8,440 | |

| Bad debt expense | $8,440 | ||

| (The reinstate the account of Person KQ) | |||

| October 16 | Cash | $8,440 | |

| Accounts receivable – Person KQ | $8,440 | ||

| (To record collection of cash on account) | |||

| December 31 | Bad debt expense | $24,995 | |

| Account receivable – Person WD | $4,600 | ||

| Account receivable – Person GG | $3,600 | ||

| Account receivable – Person AK | $7,150 | ||

| Account receivable – Person SP | $2,975 | ||

| Account receivable – Person NS | $6,630 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| December 31 | No entry is required | ||

Table (1)

Explanation of Solution

Accounts receivable: Accounts receivable refers to the amounts to be received within a short period from customers upon the sale of goods and services on account. In other words, accounts receivable are amounts customers owe to the business. Accounts receivable is an asset of a business.

Bad debt expense: Bad debt expense is an expense account. The amounts of loss incurred from extending credit to the customers are recorded as bad debt expense. In other words, the estimated uncollectible accounts receivable are known as bad debt expense.

Direct write-off method: This method does not make allowance or estimation for uncollectible accounts, instead this method directly write-off the actual uncollectible accounts by debiting bad debt expense and by crediting accounts receivable. Under this method, accounts would be written off only when the receivables from a customer remain uncollectible.

The explanation for the transactions is as follows:

For June 8:

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased by $8,440. Hence,

- • An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited with $8,440, and

- • A decrease in accounts receivable (asset account) is credited with $8,440.

For August 14:

To record the collection of cash on account, cash account must be increased and accounts receivable must be decreased by $3,000.

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased by $9,500. Hence,

- • An increase in cash (asset account) is debited with $3,000

- • An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited with $9,500, and

- • A decrease in accounts receivable (asset account) is credited with

For October 16:

On October 16, the company has recovered $8,440 from Person KQ in full, whose account is previously written off as uncollectible. Hence, company required reversing the entry, which is previously written off as uncollectible receivables. Hence,

- • Accounts receivable (asset account) is debited to increase its balance by $8,440, and

- • Bad debt expense (stockholders’ equity) is credited to decrease its balance by $8,440.

Now, the collection of cash on account, increases cash and decreases accounts receivable by $8,440, as company has collected its receivables. Hence,

- • An increase in cash (asset account) is debited with $8,440, and

- • A decrease in accounts receivable (asset account) is credited with $8,440.

For December 31:

To record this write-off of uncollectible receivables under direct write-off method, bad debt expense must be recognized as well as increased, and accounts receivable must be decreased. Hence,

- • An increase in bad debt expense (decreases the stockholders’ equity accounts) is debited, and

- • A decrease in accounts receivable (asset account) is credited.

Adjusting entry is not required under direct write off method, since this method used to write off the accounts receivable accounts only when it is determined to be worthless.

B.

Prepare journal entry to record the transactions under allowance method (Aging analysis method).

Answer to Problem 14E

Journalize the transactions of Company RT under allowance method.

| Date | Particulars | Debit | Credit |

| June 8 | Allowance for doubtful accounts | $8,440 | |

| Account receivable – Person KQ | $8,440 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| August 14 | Cash | $3,000 | |

| Allowance for doubtful accounts | $9,500 | ||

| Account receivable – Person RO | $12,500 | ||

| (To record the cash collection and write-off of remaining uncollectible account receivable ) | |||

| October 16 | Accounts receivable – Person KQ | $8,440 | |

| Allowance for doubtful accounts | $8,440 | ||

| (The reinstate the account of Person S) | |||

| October 16 | Cash | $8,440 | |

| Accounts receivable – Person KQ | $8,440 | ||

| (To record collection of cash on account) | |||

| December 31 | Allowance for doubtful accounts | $24,955 | |

| Account receivable – Person WD | $4,600 | ||

| Account receivable – Person GG | $3,600 | ||

| Account receivable – Person AK | $7,150 | ||

| Account receivable – Person SP | $2,975 | ||

| Account receivable – Person NS | $6,630 | ||

| (To record the write-off of uncollectible account receivable ) | |||

| December 31 | Bad debt expense (1) | $45,545 | |

| Allowance for doubtful accounts | $45,545 | ||

| (To adjust the allowance for doubtful accounts) | |||

Table (2)

Explanation of Solution

Allowance method: It is a method for accounting bad debt expense, where amount of uncollectible accounts receivables are estimated and recorded at the end of particular period. Under this method, bad debts expenses are estimated and recorded prior to the occurrence of actual bad debt, in compliance with matching principle by using the allowance for doubtful account.

Two methods to estimate uncollectible accounts under allowance method are:

- • Percentage of sales method, and

- • Analysis of receivables method.

Analysis of receivables method: A method of determining the estimated uncollectible receivables based on the age of individual accounts receivable is known as analysis of receivables method. This method is otherwise known as aging of receivables method. Under analysis of receivables method, estimated bad debts would be treated as the desired adjusted balance for allowance for doubtful accounts.

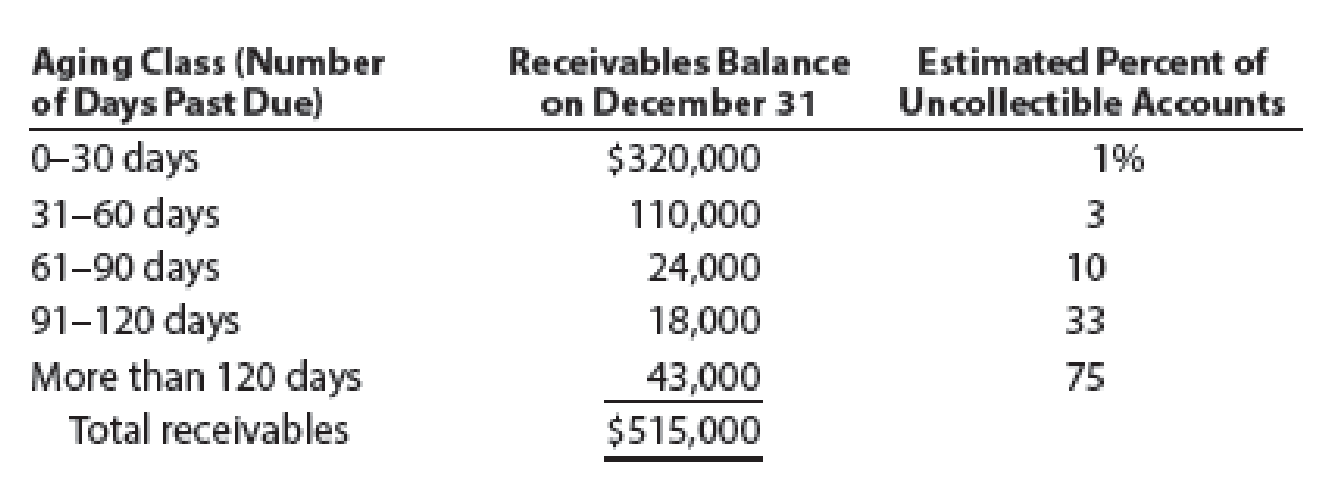

Working note 1: Estimate the balance of the allowance for doubtful accounts as of December 31 using aging schedule.

| Age interval | Balance | Estimated uncollectible accounts | |

| Percent | Amount | ||

| 1-30 days past due | $320,000 | 1% | $3,200 |

| 31-60 days past due | $110,000 | 3% | $3,300 |

| 61-90 days past due | $24,000 | 10% | $2,400 |

| 91-120 days past due | $18,000 | 33% | $5,940 |

| More than 120 days | $43,000 | 75% | $32,250 |

| Total | $515,000 | $47,090 | |

Table (3)

The aging of accounts receivable indicates that the total estimated allowance for doubtful accounts as of December 31 is $47,090.

Prepare T-account for allowance for doubtful accounts to determine the unadjusted balance of allowance account.

| Allowance for doubtful accounts | |||||

| Date | Particulars | Debit | Date | Particulars | Credit |

| June 8 | Accounts receivable | $8,440 | January 1 | Beginning balance | $36,000 |

| August 14 | Accounts receivable | $9,500 | October 16 | Accounts receivable | $8,440 |

| December 31 | Accounts receivable | $24,955 | |||

| Total | $42,895 | Total | $44,440 | ||

| Ending balance | $1,545 | ||||

Table (4)

Now, calculate the amount of bad debt expense to be recorded in adjusting entry.

For June 8:

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased by $8,440. Hence,

- • A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited with $8,440.

- • A decrease in accounts receivable (asset account) is credited with $8,440.

For August 14:

To record the collection of cash on account, cash account must be increased and accounts receivable must be decreased by $3,000.

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased by $9,500. Hence,

- • An increase in cash (asset account) is debited with $3,000,

- • A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited with $9,500, and

- • A decrease in accounts receivable (asset account) is credited with

For October 16:

On October 16, Company RT has recovered $8,440 from Person KQ in full, whose account is previously written off as uncollectible. Hence, company should reverse the entry, which is previously written off as uncollectible receivables. Hence,

- • Accounts receivable (asset account) is debited to increase its balance by $8,440, and

- • Allowance for doubtful accounts (contra-asset account) is credited to increase its balance by $8,440.

Now, the collection of cash on account, increases cash and decreases accounts receivable by $8,440, as company has collected its receivables. Hence,

- • An increase in cash (asset account) is debited with $8,440, and

- • A decrease in accounts receivable (asset account) is credited with $8,440.

For December 31:

To record this write-off of uncollectible receivables under allowance method, both allowance for doubtful accounts and accounts receivable must be decreased.

- • A decrease in Allowance for doubtful accounts (contra-asset accounts) is debited and,

- • A decrease in accounts receivable (asset account) is credited.

Adjusting entry is required at the end of the year, under allowance method. Aging receivables method is followed; hence estimated bad debts would be treated as ending balance of allowance account. Allowance for doubtful accounts (contra asset account) normal balance is a credit balance, it is calculated and determined that the unadjusted balance of Allowance for doubtful accounts as of December 31 is a credit of $1,545. It is calculated that total estimated allowance for doubtful accounts as of December 31 is $47,090. Hence, to bring the allowance for doubtful account balance from a credit of $1,545 to a credit of $47,090, it is required to increase bad debt expense and allowance for doubtful accounts by $45,545.

Hence, an increase in bad debt expense (decrease in stockholders’ equity account) is debited with $45,545 and an increase in allowance for doubtful accounts (contra asset account) is credited with $$45,545.

C.

Determine whether net income of Company RT is higher or lower under the direct-write off method than allowance method.

Explanation of Solution

Determine whether net income of Company RT is higher or lower under the direct-write off method than allowance method.

| Bad debt expense under: | Amount |

| Allowance method (1) | $45,545 |

| Direct-write off method (2) | $34,445 |

| Difference | $11,090 |

Table (5)

Bad debt expense under allowance method is higher than direct write-off method. Increase in expense decreases the net income. Hence, Company RT’s net income would have been higher under the direct write off method than the allowance method by $11,090.

Working note 2: Prepare T-account for bad debt expense account (for direct write off method).

| Bad debt expense account | |||||

| Date | Particulars | Debit | Date | Particulars | Credit |

| June 8 | Accounts receivable | $8,840 | October 16 | Accounts receivable | $8,440 |

| August 14 | Accounts receivable | $9,500 | |||

| December 31 | Accounts receivable | $24,955 | |||

| Total | $42,895 | Total | $8,440 | ||

| Ending balance | $34,445 | ||||

Table (6)

Want to see more full solutions like this?

Chapter 8 Solutions

Financial And Managerial Accounting

- The following accounts receivable information pertains to Marshall Inc. Determine the estimated uncollectible bad debt from Marshall Inc. using the balance sheet aging of receivables method, and record the year-end adjusting journal entry for bad debt.arrow_forwardBristax Corporation recorded $1,385,660 in credit sales for the year, and $732,410 in accounts receivable. The uncollectible percentage is 3.1% for the income statement method and 4.5% for the balance sheet method. A. Record the year-end adjusting entry for 2018 bad debt using the income statement method. B. Record the year-end adjusting entry for 2018 bad debt using the balance sheet method. C. Assume there was a previous debit balance in Allowance for Doubtful Accounts of $20,550; record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method. D. Assume there was a previous credit balance in Allowance for Doubtful Accounts of $17,430; record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method.arrow_forwardEntries for bad debt expense under the direct write-off and allowance methods Casebolt Company wrote off the following accounts receivable as uncollectible for the first year of its operations ending December 31: A. Journalize the write-offs under the direct write-off method. B. Journalize the write-offs under the allowance method. Also, journalize the adjusting entry for uncollectible accounts. The company recorded 5,250,000 of credit sales during the year. Based on past history and industry averages, % of credit sales are expected to be uncollectible. C. How much higher (lower) would Casebolt Companys net income have been under the direct write-off method than under the allowance method?arrow_forward

- Ink Records recorded $2,333,898 in credit sales for the year and $1,466,990 in accounts receivable. The uncollectible percentage is 3% for the income statement method and 5% for the balance sheet method. A. Record the year-end adjusting entry for 2018 bad debt using the income statement method. B. Record the year-end adjusting entry for 2018 bad debt using the balance sheet method. C. Assume there was a previous credit balance in Allowance for Doubtful Accounts of $20,254; record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method.arrow_forwardJars Plus recorded $861,430 in credit sales for the year and $488,000 in accounts receivable. The uncollectible percentage is 2.3% for the income statement method, and 3.6% for the balance sheet method. A. Record the year-end adjusting entry for 2018 bad debt using the income statement method. B. Record the year-end adjusting entry for 2018 bad debt using the balance sheet method. C. Assume there was a previous debit balance in Allowance for Doubtful Accounts of $10,220, record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method. D. Assume there was a previous credit balance in Allowance for Doubtful Accounts of $5,470, record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method.arrow_forwardCasebolt Company wrote off the following accounts receivable as uncollectible for the first year of its operations ending December 31: a. Journalize the write-offs under the direct write-off method. b. Journalize the write-offs under the allowance method. Also, journalize the adjusting entry for uncollectible accounts. The company recorded 5,250,000 of credit sales during the year. Based on past history and industry averages, % of credit sales are expected to be uncollectible. c. How much higher (lower) would Casebolt Companys net income have been under the direct write-off method than under the allowance method?arrow_forward

- Entries for Bad Debt Expense Under the Direct Write-Off and Allowance Method The following selected transactions were taken from the records of Rustic Tables Company for the year ending December 31: June 8. Wrote off account of Kathy Quantel, $4,710. Aug. 14. Received $3,340 as partial payment on the $8,430 account of Rosalie Oakes. Wrote off the remaining balance as uncollectible. Oct. 16. Received the $4,710 from Kathy Quantel, which had been written off on June 8. Reinstated the account and recorded the cash receipt. Dec. 31. Wrote off the following accounts as uncollectible (record as one journal entry): Wade Dolan $1,370 Greg Gagne 850 Amber Kisko 3,250 Shannon Poole 1,880 Niki Spence 520 Dec. 31 If necessary, record the year-end adjusting entry for the uncollectible accounts.The company prepared the following aging schedule for its accounts receivable: Aging Class (Numberof Days Past Due) Receivables Balanceon December 31 Estimated Percent…arrow_forwardFunnel Direct recorded $1,344,780 in credit sales for the year and $698,455 in accounts receivable. The uncollectible percentage is 4.4% for the income statement method and 4% for the balance sheet method. A. Record the year-end adjusting entry for 2018 bad debt using the income statement method. B. Record the year-end adjusting entry for 2018 bad debt using the balance sheet method. C. Assume there was a previous credit balance in Allowance for Doubtful Accounts of $13,788; record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method. If an amount box does not require an entry, leave it blank. Round your answers to two decimal places. А. Dec. 31 To record bad debt, income statement method В. Dec. 31 To record bad debt, balance sheet method C. Dec. 31 To record bad debt, income statement method, previous credit balance Dec. 31 To record bad debt, balance sheet method, previous credit balancearrow_forwardFunnel Direct recorded $1,341,780 in credit sales for the year and $699,455 in accounts receivable. The uncollectible percentage is 4.4% for the income statement method and 4% for the balance sheet method. A. Record the year-end adjusting entry for 2018 bad debt using the income statement method. B. Record the year-end adjusting entry for 2018 bad debt using the balance sheet method. C. Assume there was a previous credit balance in Allowance for Doubtful Accounts of $13,588; record the year-end entry for bad debt using the income statement method, and then the entry using the balance sheet method. If an amount box does not require an entry, leave it blank. Round your answers to two decimal places. A. Dec. 31 - Select - - Select - - Select - - Select - To record bad debt, income statement method B. Dec. 31 - Select - - Select - - Select - - Select - To record bad debt, balance sheet method C. Dec. 31 - Select - - Select -…arrow_forward

- Entries for Bad Debt Expense under the Direct Write-Off and Allowance Methods The following selected transactions were taken from the records of Shipway Company for the first year of its operations ending December 31: Apr. 13. Wrote off account of Dean Sheppard, $8,450. May 15. Received $500 as partial payment on the $7,100 account of Dan Pyle. Wrote off the remaining balance as uncollectible. July 27. Received $8,450 from Dean Sheppard, whose account had been written off on April 13. Reinstated the account and recorded the cash receipt. Dec. 31. Wrote off the following accounts as uncollectible (record as one journal entry): Paul Chapman $2,225 Duane DeRosa 3,550 Teresa Galloway 4,770 Ernie Klatt 1,275 Marty Richey 1,690 31. If necessary, record the year-end adjusting entry for uncollectible accounts. If no entry is required, select "No entry" and leave the amount boxes blank. If an amount box does not require an entry, leave it blank. a.…arrow_forwardEntries for Bad Debt Expense under the Direct Write-Off and Allowance Methods The following selected transactions were taken from the records of Shipway Company for the first year of its operations ending December 31: Apr. 13. Wrote off account of Dean Sheppard, $2,370. May 15. Received $1,190 as partial payment on the $3,150 account of Dan Pyle. Wrote off the remaining balance as uncollectible. July 27. Received $2,370 from Dean Sheppard, whose account had been written off on April 13. Reinstated the account and recorded the cash receipt. Dec. 31. Wrote off the following accounts as uncollectible (record as one journal entry): Paul Chapman $1,590 Duane DeRosa 1,190 Teresa Galloway 710 Ernie Klatt 1,000 Marty Richey 360 31. If necessary, record the year-end adjusting entry for the uncollectible accounts. If no entry is required, select "No entry" and leave the amount boxes blank. If an amount box does not require an entry, leave it blank. a.…arrow_forwardRequired:1. Prepare journal entries for each transaction.2. Prepare the Allowance for Uncollectible and the Accounts Receivable accounts based on theinformation presented and balance off each account.3. Prepare the balance sheet extract as at Dec 31 to show the net realizable value for theAccounts Receivable.4. Assume that the aging of accounts receivable method was used by the company and that$7,050 of the accounts receivable as of December 31 were estimated to be uncollectible. Youare now required to:a. Determine the amount to be charged to uncollectible expense (show yourworkings for the computation of this figure).b. Prepare the balance sheet extract to show the net realizable value of the AccountsReceivable as at December 31arrow_forward

- Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Principles of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College