Concept explainers

Videos

(Appendix 4B) Support Department Cost Allocation

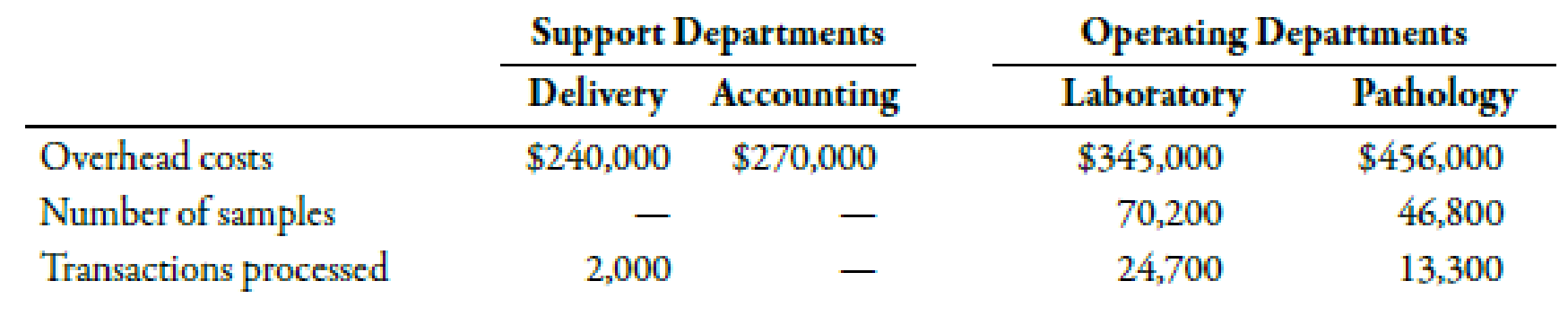

MedServices Inc. is divided into two operating departments: Laboratory and Tissue Pathology. The company allocates delivery and accounting costs to each operating department. Delivery costs include the costs of a fleet of vans and drivers that drive throughout the state each day to clinics and doctors’ offices to pick up samples and deliver them to the centrally located laboratory and tissue pathology offices. Delivery costs are allocated on the basis of number of samples. Accounting costs are allocated on the basis of the number of transactions processed. No effort is made to separate fixed and variable costs; however, only budgeted costs are allocated. Allocations for the coming year are based on the following data:

Required:

- 1. Assign the support department costs by using the direct method. (Note: Round allocation ratios to four decimal places.)

- 2. Assign the support department costs by using the sequential method, allocating accounting costs first. (Note: Round allocation ratios to four decimal places.)

1.

Calculate the assigned cost of support departments by using direct method.

Explanation of Solution

Direct Method:

Direct method implies that the unit cost must include all the factory costs. It states that the cost of support departments should not be added in the unit cost if it is not included in operating departments’ cost because they do not play any role in selling the unit or product.

Use the following formula to calculate assignment ratios on the basis of number of samples:

Laboratory department:

Substitute 70,200 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.60.

Pathology department:

Substitute 46,800 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.40.

Use the following formula to calculate assignment ratios on the basis of transactions processed:

Laboratory department:

Substitute 24,700 for transactions processed in laboratory and 38,000 for total transactions processed in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.65.

Pathology department:

Substitute 13,300 for transactions processed in laboratory and 38,000 for total transactions processed in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.35.

Assign cost of support departments to the operating departments:

| Support departments | Operating departments | |||

| Delivery($) | Accounting($) | Laboratory($) | Pathology($) | |

| Direct costs | 240,000 | 270,000 | 345,000 | 456,000 |

| Delivery1 | -240,000 | 144,000 | 96,000 | |

| Accounting1 | -270,000 | 175,500 | 94,500 | |

| Total | 0 | 0 | 664,500 | 646,500 |

Table (1)

Working Note:

1. Calculation of assigned cost of support department to operating department:

| Account Title |

Assignment ratio A |

Support department cost($) B |

Assigned cost($) |

| Delivery cost: | |||

| Laboratory | 0.6000 | 240,000 | 144,000 |

| Pathology | 0.4000 | 240,000 | 96,000 |

| Accounting: | |||

| Laboratory | 0.65 | 270,000 | 175,500 |

| Pathology | 0.35 | 270,000 | 94,500 |

Table (2)

2.

Calculate the assigned cost of support departments by using sequential method and allocate accounting costs first.

Explanation of Solution

Sequential Method:

Sequential method recognizes that there is possible interaction between the support departments. However, it does not account for such interaction in full which makes it more accurate as compared to the direct method.

Use the following formula to calculate cost assignment ratios on the basis of number of transactions processed:

Delivery:

Substitute 2,000 for transactions processed in delivery and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for delivery is 0.0500.

Laboratory department:

Substitute 24,700 for transactions processed in laboratory and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for laboratory department is 0. 6175.

Pathology department:

Substitute 13,300 for transactions processed in pathology and 40,000 for total transactions processed in the above formula.

Therefore, the cost assignment ratio for pathology department is 0.3325.

Use the following formula to calculate assignment ratios on the basis of number of samples:

Laboratory department:

Substitute 70,200 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for laboratory department is 0.60.

Pathology department:

Substitute 46,800 for number of samples in laboratory and 117,000 for total samples in operating department in the above formula.

Therefore, the assignment ratio for pathology department is 0.40.

Assign cost of support departments to the operating departments:

| Support departments | Operating departments | |||

| Delivery($) | Accounting($) | Laboratory($) | Pathology($) | |

| Direct costs | 240,000 | 270,000 | 345,000 | 456,000 |

| Accounting2 | 13,500 | 166,725 | 89,775 | |

| Delivery2 | -253,500 | -270,000 | 152,100 | 101,400 |

| Total | 0 | 0 | 663,825 | 647,175 |

Table (3)

Working Note:

2. Calculation of assigned cost of support department:

| Account Title |

Assignment ratio A |

Support department cost($) B |

Assigned cost($) |

| Accounting: | |||

| Delivery | 0.0500 | 270,000 | 13,500 |

| Laboratory | 0.6175 | 270,000 | 166,725 |

| Pathology | 0.3325 | 270,000 | 89,775 |

| Delivery cost: | |||

| Laboratory | 0.60 | 253,500 | 152,100 |

| Pathology | 0.40 | 253,500 | 101,400 |

Table (4)

Want to see more full solutions like this?

Chapter 4 Solutions

Managerial Accounting: The Cornerstone of Business Decision-Making

- Pelder Products Company manufactures two types of engineering diagnostic equipment used in construction. The two products are based upon different technologies, X-ray and ultrasound, but are manufactured in the same factory. Pelder has computed the manufacturing cost of the X-ray and ultrasound products by adding together direct materials, direct labor, and overhead cost applied based on the number of direct labor hours. The factory has three overhead departments that support the single production line that makes both products. Budgeted overhead spending for the departments is as follows: Pelders budgeted manufacturing activities and costs for the period are as follows: The budgeted cost to manufacture one ultrasound machine using the activity-based costing method is: a. 225. b. 264. c. 293. d. 305.arrow_forwardA manufacturing company has two service and two production departments. Human Resources and Machine Repair are the service departments. The production departments are Grinding and Polishing. The following data have been estimated for next years operations: The direct charges identified with each of the departments are as follows: The human resources department services all departments of the company, and its costs are allocated using the numbers of employees within each department, while machine repair costs are allocable to Grinding and Polishing on the basis of machine hours. 1. Distribute the service department costs, using the direct method. 2. Distribute the service department costs, using the sequential distribution method, with the department servicing the greatest number of other departments distributed first.arrow_forwardCharlies Wood Works produces wood products (e.g., cabinets, tables, picture frames, and so on). Production departments include Cutting and Assembly. The Janitorial and Security departments support the Cutting and Assembly departments. The Assembly Department spans about 46,400 square feet and holds assets valued at about 60,000. The Cutting Department spans about 33,600 square feet and holds assets valued at about 140,000. Charlies Wood Works allocates support department costs using the direct method. If costs from the Janitorial Department are allocated based on square feet and costs from the Security Department are allocated based on asset value, determine (a) the percentage of Janitorial costs that should be allocated to the Assembly Department and (b) the percentage of Security costs that should be allocated to the Cutting Department.arrow_forward

- Compton Information Services, Inc., has two service departments: human resources and billing. Compton's operating departments, organized according to the special industry each department serves, are health care, retail, and legal services. The billing department supports only the three operating departments, but the human resources department supports all operating departments and the billing department. Other relevant information follows. Human Health Legal Resources Billing Care Retail Services Number of employees 10 20 80 60 40 Annual cost* $4,800,000 $6,200,000 $720,000 $1,428,000 $6,000,000 $9,000,000 $2,800,000 $4,800,000 Annual revenue *This is the operating cost before allocating service department costs. Required a. Allocate service department costs to operating departments, assuming that Compton adopts the step method. The company uses the number of employees as the base for allocating human resources department costs and department annual revenue as the base for allocating…arrow_forwardStoltz Corporation uses the direct method to allocate service department costs to operating departments. The company has two service departments, Data Processing and Personnel, and two operating departments, Assembly and Finishing. Service Department Data Processing $ 54,365 Operating Department Assembly $ 314,500 Personnel Finishing $ 677,630 $ 34,560 Departmental costs Computer workstations Employees 53 35 68 63 47 30 75 60 Data Processing Department costs are allocated on the basis of computer workstations and Personnel Department costs are allocated on the basis of employees. The total amount of Data Processing Department cost allocated to the two operating departments is closest to: Multiple Choice $54,365 $26.145 $19,200 $28,220arrow_forwardPleasant Stay Medical Inc. wishes to determine its product costs. Pleasant Stay offers a variety of medical procedures (operations) that are considered its “products.” The overhead has been separated into three major activities. The annual estimated activity costs and activity bases follow: Activity Budgeted Activity Cost Activity Base Scheduling and admitting $432,000 Number of patients Housekeeping 4,212,000 Number of patient days Nursing 5,376,000 Weighted care unit Total costs $10,020,000 Total “patient days” are determined by multiplying the number of patients by the average length of stay in the hospital. A weighted care unit (wcu) is a measure of nursing effort used to care for patients. There were 192,000 weighted care units estimated for the year. In addition, Pleasant Stay estimated 6,000 patients and 27,000 patient days for the year. (The average patient is expected to have a a little more than a…arrow_forward

- Solomon Information Services, Incorporated, has two service departments: human resources and billing. Solomon's operating departments, organized according to the special Industry each department serves, are health care, retall, and legal services. The billing department supports only the three operating departments, but the human resources department supports all operating departments and the billing department. Other relevant information follows. Number of employees Annual cost* Annual revenue Req A1 Department Human Resources Billing Health Care Retail Req A2 Legal Services Total 20 $ 900,000 Complete this question by entering your answers in the tabs below. Allocation Rate Req B1 *This is the operating cost before allocating service department costs. Required a. Allocate service department costs to operating departments, assuming that Solomon adopts the step method. The company uses the number of employees as the base for allocating human resources department costs and department…arrow_forwardStoltz Corporation uses the direct method to allocate service department costs to operating departments. The company has two service departments, Data Processing and Personnel, and two operating departments, Assembly and Finishing. Service Department Data Processing $ 26,488 Operating Department Assembly $ 188,980 Finishing $ 506,960 Personnel $ 18,630 Departmental costs Computer workstations Employees 37 12 45 41 35 11 46 35 Data Processing Department costs are allocated on the basis of computer workstations and Personnel Department costs are allocated on the basis of employees. The total amount of Data Processing Department cost allocated to the two operating departments is closest to: Multiple Choice $23,245 $26,488 $61,567 $16,874arrow_forwardCompton Information Services, Inc., has two service departments: human resources and billing. Compton's operating departments, organized according to the special industry each department serves, are health care, retail, and legal services. The billing department supports only the three operating departments, but the human resources department supports all operating departments and the billing department. Other relevant information follows. Health Legal Services Human Resources Billing Care Retail Number of employees Annual cost* 10 20 80 60 40 $6,000,000 $9,000,000 $720,000 $1,428,000 $4,800,000 $6,200,000 $2,800,000 $4,800,000 Annual revenue *This is the operating cost before allocating service department costs. Required a. Allocate service department costs to operating departments, assuming that Compton adopts the step method. The company uses the number of employees as the base for allocating human resources department costs and department annual revenue as the base for allocating…arrow_forward

- Compton Information Services, Inc., has two service departments: human resources and billing. Compton's operating departments, organized according to the special industry each department serves, are health care, retail, and legal services. The billing department supports only the three operating departments, but the human resources department supports all operating departments and the billing department. Other relevant information follows. Health Legal Services Human Resources Billing Care Retail Number of employees 10 20 80 60 40 Annual cost* $720,000 $1,428,000 $6,000,000 $9,000,000 $4,800,000 $6,200,000 $2,800,000 $4,800,000 Annual revenue *This is the operating cost before allocating service department costs. Required a. Allocate service department costs to operating departments, assuming that Compton adopts the step method. The company uses the number of employees as the base for allocating human resources department costs and department annual revenue as the base for allocating…arrow_forwardUniversity Printers has two service departments (Maintenance and Personnel) and two operating departments (Printing and Developing). Management has decided to allocate maintenance costs on the basis of machine-hours in each department and personnel costs on the basis of labor-hours worked by the employees in each. The following data appear in the company records for the current period: Maintenance Personnel Developing Printing 1,400 Machine-hours 1,400 4,200 Labor-hours 800 800 3,200 Department 'direct costs $2,400 $12,400 $13,400 $10,700 Required: Use the direct method to allocate these service department costs to the operating departments. (Negative amounts should be indicated by a minus sign. Do not round intermediate calculations.) Answer is not complete. Maintenance Personnel Printing Developing Service department costs $2$ 2,400 $ 12,400 O Maintenance allocation (2,400) O 600 1,800 V Personnel allocation 2,480 9,920 Total costs allocated $ 2$ 12,400 $ 3,080 $24 11,720arrow_forwardSolomon Information Services, Incorporated, has two service departments: human resources and billing. Solomon's operating departments, organized according to the special Industry each department serves, are health care, retall, and legal services. The billing department supports only the three operating departments, but the human resources department supports all operating departments and the billing department. Other relevant information follows. Number of employees Annual cost Annual revenue Req A1 Human Resources Department Reg A2 Billing Health Care Retail Legal Services Total *This is the operating cost before allocating service department costs. Allocation Rate 20 Req B1 $ 900,000 Complete this question by entering your answers in the tabs below. x X Billing Required a. Allocate service department costs to operating departments, assuming that Solomon adopts the step method. The company uses the number of employees as the base for allocating human resources department costs and…arrow_forward

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning

Managerial Accounting: The Cornerstone of Busines...AccountingISBN:9781337115773Author:Maryanne M. Mowen, Don R. Hansen, Dan L. HeitgerPublisher:Cengage Learning Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning

Principles of Cost AccountingAccountingISBN:9781305087408Author:Edward J. Vanderbeck, Maria R. MitchellPublisher:Cengage Learning Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub

Managerial AccountingAccountingISBN:9781337912020Author:Carl Warren, Ph.d. Cma William B. TaylerPublisher:South-Western College Pub