Concept explainers

Videos

The unadjusted

| PS Music Adjusted Trial Balance July 31, 2018 | |||

| Account No. | Debit Balances | Credit Balances | |

| Cash................................................. | 11 | 9,945 | |

| Accounts Receivable................................... | 12 | 4,150 | |

| Supplies.............................................. | 14 | 275 | |

| Prepaid Insurance..................................... | 15 | 2,475 | |

| Office Equipment..................................... | 17 | 7,500 | |

| 18 | 50 | ||

| Accounts Payable..................................... | 21 | 8,350 | |

| Wages Payable........................................ | 22 | 140 | |

| Unearned Revenue.................................... | 23 | 3,600 | |

| Common Stock....................................... | 31 | 9,000 | |

| Dividends............................................ | 33 | 1,750 | |

| Fees Earned........................................... | 41 | 21,200 | |

| Music Expense........................................ | 54 | 3,610 | |

| Wages Expense....................................... | 50 | 2,940 | |

| Office Rent Expense................................... | 51 | 2,550 | |

| Advertising Expense................................... | 55 | 1,500 | |

| Equipment Rent Expense.............................. | 52 | 1,375 | |

| Utilities Expense...................................... | 53 | 1,215 | |

| Supplies Expense...................................... | 56 | 925 | |

| Insurance Expense.................................... | 57 | 225 | |

| Depreciation Expense................................. | 58 | 50 | |

| Miscellaneous Expense................................ | 59 | 1,855 | |

| 42,340 | 42,340 | ||

Instructions

1. (Optional) Using the data from Chapter 3, prepare an end-of-period spreadsheet.

2. Prepare an income statement, a retained earnings statement, and a

3. Journalize and

4. Prepare a post-dosing trial balance.

(1)

Spreadsheet:

A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

Statement of retained earnings: This statement reports the beginning retained earnings and all the changes which led to ending retained earnings. Net income from income statement is added to and dividends are deducted from beginning retained earnings to arrive at the end result, ending retained earnings.

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr) and,

- The credit side (Cr).

Closing entries:

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts. It is passed at the end of the accounting period, to transfer the final balance.

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

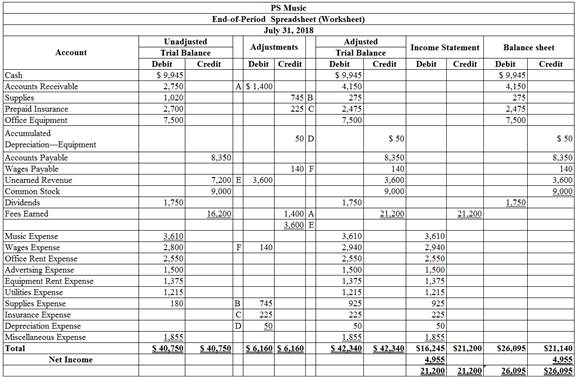

To prepare: An end-of-period spreadsheet.

Explanation of Solution

An end-of-period spreadsheet is prepared as follows:

Figure (1)

Hence, the end-of-period spreadsheet is prepared and completed.

(2)

To Prepare: An income statement for the year ended July 31, 2018.

Explanation of Solution

An income statement for the year ended July 31, 2018 is as follows:

| PS Music | ||

| Income Statement | ||

| For July 31, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 21,200 | |

| Expenses: | ||

| Music Expense | 3,610 | |

| Wages Expense | 2,940 | |

| Office Rent Expense | 2,550 | |

| Advertising Expense | 1,500 | |

| Equipment Rent Expense | 1,375 | |

| Utilities Expense | 1,215 | |

| Supplies Expense | 925 | |

| Insurance Expense | 225 | |

| Depreciation Expense | 50 | |

| Miscellaneous Expense | 1,855 | |

| Total Expenses | 16,245 | |

| Net Income | $4,955 | |

Table (1)

Hence, the net income of PS Music for the year ended July 31, 2018 is $4,955.

To Prepare: The statement of owners’ equity for the year ended July 31, 2018.

Explanation of Solution

The statement of retained earnings for the year ended July 31, 2018 is as follows:

| PS Music | ||

| Statement of Retained earnings | ||

| For the Year Ended July 31, 2018 | ||

| Particulars | Amount ($) | Amount ($) |

| Retained earnings, June 1, 2018 | 0 | |

| Add: Net income | 4,955 | |

| Less: Dividends | (1,750) | |

| Change in retained earnings | 3,205 | |

| Retained earnings, July 31, 2018 | $3,205 | |

Table (2)

Hence, owners’ equity for the year ended July 31, 2018 is $3,205.

To Prepare: The balance sheet of PS Music at July 31, 2018.

Explanation of Solution

The balance sheet of PS Music at July 31, 2018 is prepared as follows:

| PS Music | ||

| Balance Sheet | ||

| At July 31, 2018 | ||

| Assets | ||

| Current Assets: | $ | $ |

| Cash | 9,945 | |

| Accounts Receivable | 4,150 | |

| Supplies | 275 | |

| Prepaid Insurance | 2,475 | |

| Total Current Assets | 16,845 | |

| Property, plant and equipment: | ||

| Office Equipment | 7,500 | |

| Less: Accumulated Depreciation | 50 | |

| Total Plant Assets | 7,450 | |

| Total Assets | $24,295 | |

| Liabilities | ||

| Current Liabilities: | ||

| Accounts Payable | 8,350 | |

| Salaries Payable | 140 | |

| Unearned Rent | 3,600 | 12,090 |

| Total Liabilities | ||

| Stock holders’ Equity | ||

| Common Stock | 9,000 | |

| Retained Earnings | 3,205 | |

| Total Stock holders’ Equity | 12,205 | |

| Total Liabilities and Stock holders’ Equity | $24,295 | |

Table (3)

It is one of the financial statements, which shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the company has enough assets to pay off its liabilities.

Therefore, the total assets and total liabilities plus owners’ equity of PS Music at July 31, 2018 is $24,295.

(3)

To Journalize: The closing entries for PS Music.

Explanation of Solution

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| July 31, 2018 | Fees Earned | 41 | 21,200 | |

| Income Summary | 34 | 21,200 | ||

| (To record the closure of revenues account ) | ||||

| July 31 | Income Summary | 34 | 16,245 | |

| Wages Expense | 50 | 2,940 | ||

| Office Rent Expense | 51 | 2,550 | ||

| Equipment Rent Expense | 52 | 1,375 | ||

| Utilities Expense | 53 | 1,215 | ||

| Music Expense | 54 | 3,610 | ||

| Advertising Expense | 55 | 1,500 | ||

| Supplies Expense | 56 | 925 | ||

| Insurance Expense | 57 | 225 | ||

| Depreciation Expense | 58 | 50 | ||

| Miscellaneous Expense | 59 | 1,855 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to income summary account) | ||||

| July 31 | Income Summary | 34 | 4,955 | |

| Retained earnings | 32 | 4,955 | ||

| (To record the closure of net income from income summary to retained earnings) | ||||

| Retained earnings | 32 | 1,750 | ||

| Dividends | 33 | 1,750 | ||

| (To record the closure of dividend to retained earnings) | ||||

Table (4)

Fees earned account has a normal credit balance of $21,200 in total, now to close this account, the fees earned account must be debited with $21,200 and, income summary account must be credited with $21,200.

- In this closing entry, the fees earned account balance is being transferred to the income summary account, to bring the revenues account balance to zero.

- Thereby, the income summary account balance gets increased by $21,200 and, the revenue account balance gets decreased by $21,200.

All expenses accounts have a normal debit balance, the total of expenses are $16,245 have to be closed by transferring these account balances to the income summary account. All expenses account must be credited, and the income summary account must be debited with $ 16,245.

- In this closing entry, all the expenses account balances are transferred to the income summary account, to bring the expenses account balances to zero.

- Thereby, both the income summary account, and the expenses account balances get decreased by $16,245.

Determined amount balance of income summary is $4,955, which has to be closed by debiting the income summary account with $4,955, and crediting the retained earnings account with $4,955.

- In this closing entry, the income summary account balance is being transferred to the retained earnings account, to bring the income summary account balance to zero.

- Thereby, the income summary account gets decreased, and the retained earnings account balance gets increased by $4,955.

Dividends account has a normal debit balance of $1,750, now to close this account, retained earnings account must be debited with $1,750 and, dividend account must be credited with $1,750.

- In this closing entry, the dividend account balance is being transferred to the retained earnings account, to bring the dividend account balance to zero.

- Thereby, the retained earnings account balance gets increased by $1,750 and, the dividend account balance gets decreased by $1,750

To post: The closing entries of PS Music accounts in the appropriate balance column of a four-column account.

Explanation of Solution

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 3,920 | |||

| 1 | 1 | 5,000 | 8,920 | ||||

| 1 | 1 | 1,750 | 7,170 | ||||

| 1 | 1 | 2,700 | 4,470 | ||||

| 2 | 1 | 1,000 | 5,470 | ||||

| 3 | 1 | 7,200 | 12,670 | ||||

| 3 | 1 | 250 | 12,420 | ||||

| 4 | 1 | 900 | 11,520 | ||||

| 8 | 1 | 200 | 11,320 | ||||

| 11 | 1 | 1,000 | 12,320 | ||||

| 13 | 1 | 700 | 11,620 | ||||

| 14 | 1 | 1,200 | 10,420 | ||||

| 16 | 2 | 2,000 | 12,420 | ||||

| 21 | 2 | 620 | 11,800 | ||||

| 22 | 2 | 800 | 11,000 | ||||

| 23 | 2 | 750 | 11,750 | ||||

| 27 | 2 | 915 | 10,835 | ||||

| 28 | 2 | 1,200 | 9,635 | ||||

| 29 | 2 | 540 | 9,095 | ||||

| 30 | 2 | 500 | 9,595 | ||||

| 31 | 2 | 3,000 | 12,595 | ||||

| 31 | 2 | 1,400 | 11,195 | ||||

| 31 | 2 | 1,250 | 9,945 | ||||

Table (5)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 1,000 | |||

| 2 | 1 | 1,000 | |||||

| 23 | 2 | 1,750 | 1,750 | ||||

| 30 | 2 | 1,000 | 2,750 | ||||

| 31 | Adjusting | 3 | 1,400 | 4,150 | |||

Table (6)

| Account: Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 170 | |||

| 18 | 2 | 850 | 1,020 | ||||

| 31 | Adjusting | 3 | 745 | 275 | |||

Table (7)

| Account: Prepaid Insurance Account no. 15 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | 1 | 2,700 | 2,700 | |||

| 31 | Adjusting | 3 | 225 | 2,475 | |||

Table (8)

| Account: Office equipment Account no. 17 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 5 | 1 | 7,500 | 7,500 | |||

Table (9)

| Account: Accumulated Depreciation-Office equipment Account no. 18 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 31 | Adjusting | 3 | 50 | 50 | ||

Table (10)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 250 | |||

| 3 | 1 | 250 | |||||

| 5 | 1 | 7,500 | 7,500 | ||||

| 18 | 2 | 850 | 8,350 | ||||

Table (11)

| Account: Wages Payable Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 31 | Adjusting | 3 | 140 | 140 | ||

Table (12)

| Account: Unearned Revenue Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 3 | 1 | 7,200 | 7,200 | |||

| 31 | Adjusting | 3 | 3,600 | 3,600 | |||

Table (13)

| Account: Common Stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | ✓ 1 | 5,000 | ||||

| 1 | Balance | 1 | 4,000 | 9,000 | |||

Table (14)

| Account: Retained earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | |||||

| 31 | Closing | 4 | 4,955 | 4,955 | |||

| 31 | Closing | 4 | 1,750 | 3,205 | |||

Table (15)

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 31 | 2 | 1,250 | 1,750 | ||||

| 31 | Closing | 4 | 1,750 | ||||

Table (16)

| Account: Income Summary Account no. 34 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 31 | Closing | 4 | 21,200 | 21,200 | ||

| 31 | Closing | 4 | 16,245 | 4,955 | |||

| 31 | Closing | 4 | 4,955 | ||||

Table (17)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 6,200 | |||

| 11 | 1 | 1,000 | 7,200 | ||||

| 16 | 2 | 2,000 | 9,200 | ||||

| 23 | 2 | 2,500 | 11,700 | ||||

| 30 | 2 | 1,500 | 13,200 | ||||

| 31 | 2 | 3,000 | 16,200 | ||||

| 31 | Adjusting | 3 | 1,400 | 17,600 | |||

| 31 | Adjusting | 3 | 3,600 | 21,200 | |||

| 31 | Closing | 4 | 21,200 | ||||

Table (18)

| Account: Wages expense Account no. 50 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 400 | |||

| 14 | 1 | 1,200 | 1,600 | ||||

| 27 | 2 | 1,200 | 2,800 | ||||

| 31 | Adjusting | 3 | 140 | 2,940 | |||

| 31 | Closing | 4 | 2,940 | ||||

Table (19)

| Account: Office Rent expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 800 | |||

| 1 | 1 | 1,750 | 2,550 | ||||

| 31 | Closing | 4 | 2,550 | ||||

Table (20)

| Account: Equipment rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 675 | |||

| 31 | 1 | 700 | 1,375 | ||||

| 31 | Closing | 4 | 1,375 | ||||

Table (21)

| Account: Utilities expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 300 | |||

| 27 | 2 | 915 | 1,215 | ||||

| 31 | Closing | 4 | 1,215 | ||||

Table (22)

| Account: Music expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 1,590 | |||

| 21 | 2 | 620 | 2,210 | ||||

| 31 | 2 | 1,400 | 3,610 | ||||

| 31 | Closing | 4 | 3,610 | ||||

Table (23)

| Account: Advertising expense Account no. 55 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 500 | |||

| 8 | 1 | 200 | 700 | ||||

| 22 | 2 | 800 | 1,500 | ||||

| 31 | Closing | 4 | 1,500 | ||||

Table (24)

| Account: Supplies expense Account no. 56 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 180 | |||

| 22 | Adjusting | 2 | 745 | 925 | |||

| 31 | Closing | 4 | 925 | ||||

Table (25)

| Account: Insurance expense Account no. 57 | ||||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | |||

| Debit ($) | Credit ($) | |||||||

| 2018 | ||||||||

| July | 31 | Adjusting | 3 | 225 | 225 | |||

| 31 | Closing | 4 | 225 | |||||

Table (26)

| Account: Depreciation expense Account no. 58 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 31 | Adjusting | 3 | 50 | 50 | ||

| 31 | Closing | 4 | 50 | ||||

Table (27)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) |

Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 2018 | |||||||

| July | 1 | Balance | ✓ | 415 | |||

| 4 | 1 | 900 | 1,315 | ||||

| 29 | 2 | 540 | 1,855 | ||||

| 31 | Closing | 4 | 1,855 | ||||

Table (28)

(4)

To prepare: A post–closing trial balance of PS Music for July 31, 2018.

Explanation of Solution

Prepare a post–closing trial balance of PS Music for July 31, 2018 as follows:

|

PS Music Post-closing Trial Balance July, 31, 2018 |

|||

| Particulars | Account No | Debit $ | Credit $ |

| Cash | 11 | 9,945 | |

| Accounts receivable | 12 | 4,150 | |

| Supplies | 14 | 275 | |

| Prepaid insurance | 15 | 2,475 | |

| Office Equipment | 17 | 7,500 | |

| Accumulated depreciation – Office Equipment | 18 | 50 | |

| Accounts payable | 21 | 8,350 | |

| Wages payable | 22 | 140 | |

| Unearned revenue | 23 | 3,600 | |

| Common Stock | 31 | 9,000 | |

| Retained earnings | 32 | 3,205 | |

| Total | 24,345 | 24,345 | |

Table (29)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $24,345.

Want to see more full solutions like this?

Chapter 4 Solutions

CENGAGENOW FOR CORP. FINC

- Ace Company uses the Aging of receivables method to account for uncollectible accounts. Thecompany had the following balances on January 01, 2019.Part AAccounts receivable...........................................$2,800,000Allowance for uncollectible accounts...................$88,800 (credit)The company completed the following transactions during 2019. April 20-- Wrote off the balance of $1,000 from Shari Wickham’s account asuncollectible. November 27- Re-instated the account of Louis Benn and recorded the collection of$1,500 as payment in full for her account which had been written off earlier. December 31sti. Recorded the uncollectible account expense based on the aging schedule. Theschedule showed that $124,500 of accounts receivable was estimated asuncollectible.ii. Made the closing entry for the uncollectible expense account.Requirements:1. Prepare journal entries for each transaction (No narrations required)2. Prepare the Allowance for Uncollectible and the Accounts…arrow_forwardDiscussion question: Ace Company uses the Aging of receivables method to account for uncollectible accounts. The company had the following balances on January 01, 2019. Part A Accounts receivable...........................................$2,800,000 Allowance for uncollectible accounts...................$88,800 (credit) The company completed the following transactions during 2019. April 20-- Wrote off the balance of $1,000 from Shari Wickham’s account as uncollectible. November 27- Re-instated the account of Louis Benn and recorded the collection of $1,500 as payment in full for her account which had been written off earlier. December 31st- Recorded the uncollectible account expense based on the aging schedule. The schedule showed that $124,500 of accounts receivable was estimated as uncollectible. Made the closing entry for the uncollectible expense account. Requirements: Prepare journal entries for each transaction (No narrations required) Prepare the Allowance for…arrow_forward9. The adjusting journal entry to adjust the allowance for doubtful accounts as of December 31, 2020 will include a debit to doubtful accounts expense of:arrow_forward

- The adjusted Trail Balance of Saudi Gold Co Contained the following accounts at November 30, the end of the company’s fiscal year : Saudi Gold Co. Adjusted Trial Balance November 30, 2019 Dr. Cr. Cash............................................................... Sr 28,700 Accounts Receivable..................................... 33,700 Inventory........................................................ 45,000 Supplies......................................................... 1,500 Equipment...................................................... 133,000 Accumulated Depreciation—Equipment..... Sr 39,000 Notes Payable................................................ 51,000 Accounts Payable......................................... 48,500 Share Capital—Ordinary............................... 90,000 Retained…arrow_forwardAce Company uses the Aging of receivables method to account for uncollectible accounts. The company had the following balances on January 01, 2019. Part A Accounts receivable...........................................$2,800,000 Allowance for uncollectible accounts...................$88,800 (credit) The company completed the following transactions during 2019. April 20-- Wrote off the balance of $1,000 from Shari Wickham’s account as uncollectible. November 27- Re-instated the account of Louis Benn and recorded the collection of $1,500 as payment in full for her account which had been written off earlier. December 31st- Recorded the uncollectible account expense based on the aging schedule. The schedule showed that $124,500 of accounts receivable was estimated as uncollectible. Made the closing entry for the uncollectible expense account. Requirements: Prepare journal entries for each transaction (No narrations required) Prepare the Allowance for Uncollectible and the…arrow_forward1. Prepare the entry to record the write-off ofuncollectible accounts during 2019. 2. Prepare the entries to record the recovery ofthe uncollectible account during 2019 3. Prepare the entry to record bad debt expense(BDE) at the end of 2019. Ending balance ofAFDA was Rp18,200 (Cr.) 4. Determine the ending balance of AccountsReceivable as of December 31, 2019. 5. What is the net realizable value of thereceivables at the end of 2019? 6. The company has a notes receivable ofRp24,000 at January 15, 2019 for 3 months at10% interest rate. Prepare journal entry as ofApril 15, 2019, on its due date.arrow_forward

- Ace Company uses the Aging of receivables method to account for uncollectible accounts. The company had the following balances on January 01, 2019. Part A Accounts receivable...........................................$2,800,000 Allowance for uncollectible accounts...................$88,800 (credit) The company completed the following transactions during 2019. April 20--Wrote off the balance of $1,000 from Shari Wickham’s account as uncollectible. November 27- Re-instated the account of Louis Benn and recorded the collection of $1,500 as payment in full for her account which had been written off earlier. December 31st- i. Recorded the uncollectible account expense based on the aging schedule. The schedule showed that $124,500 of accounts receivable was estimated as uncollectible. ii. Made the closing entry for the uncollectible expense account. Requirements: Prepare journal entries for each transaction (No narrations required) Prepare the Allowance for Uncollectible and…arrow_forwardA edugen.wileyplus.com W WileyPLUS Bb Return to Blackboard US US Weygandt, Accounting Principles, 13th Edition, Custom WileyPLUS Course for Bronx Commun Help | System Announcements Problem 9-01A a-d (Video) At December 31, 2019, Ayayai Co. reported the following information on its balance sheet. Accounts receivable $965,100 Less: Allowance for doubtful accounts 79,700 During 2020, the company had the following transactions related to receivables. 1. Sales on account $3,692,700 2. Sales returns and allowances 49,600 3. Collections of accounts receivable 2,817,800 4. Write-offs of accounts receivable deemed uncollectible 89,600 5. Recovery of bad debts previously written off as uncollectible 27,350 Your answer is correct. Aceur me thatne neh diecouınte w ers Prepare the journal entries to record onch of tho0o fuo trnnanotionoarrow_forwardAn analysis and aging of accounts receivable of the Lucille Company at December 31, 2002, showed the following:Accounts Receivable ..................................Allowance for Doubtful Accounts (before adjustment) ................................Accounts estimated to be uncollectible ...............₱840,00 036,000 (cr )76,800Compute for the net realizable value of the accounts receivable of Lucille Company at December 31, 2002.arrow_forward

- The Trial Balance of BMR Limited contained the following accounts (alphabetically) at December 31, 2020, the end of company's fiscal year.Accounts …… …… …… …… …… …… …… Balances ($) . . . . ||| . . . . Accounts …… …… …… …… …… Balances ($)Accumulated Depreciation-Building…. …… 130000 . . . . ||| . . . . Loss on Sale of Property …. …. …. …. 7680Accumulated Depreciation-Equipment….…. 36000 . . . . ||| . . . . Merchandise Inventory …. …. ……. 230000Additional Paid in Capital-Common Stock.. 233000 . . . . ||| . . . . Mortgage Loan …. …. …. …. …. …… 114000Auditors Fee …. …. …. …. …. …. ….. ….. ….. .. 207000 . . . . ||| . . . . Rent Revenue …. …. …. …. …. …. … 53000Buildings…. …. …. …. …. …. ….. ….. ….. ….. ... 401000 . . . . ||| . . . . Retained Earnings …. …. …. …. …… 52600Cash …. …. …. …. …. …. ….. ….. ….. ….. ….. …. 204340 . . . . ||| . . . . Salaries and Wages Expense …. …. 106000Common Stock ($2 each)…. …. …. …. …. ….. 113000 . . . . ||| . . . . Sales …. …. …. …. …. …. ….. ….. …….…arrow_forwardThe Trial Balance of BMR Limited contained the following accounts (alphabetically) at December 31, 2020, the end of company's fiscal year.Accounts …… …… …… …… …… …… …… Balances ($) . . . . ||| . . . . Accounts …… …… …… …… …… Balances ($)Accumulated Depreciation-Building…. …… 130000 . . . . ||| . . . . Loss on Sale of Property …. …. …. …. 7680Accumulated Depreciation-Equipment….…. 36000 . . . . ||| . . . . Merchandise Inventory …. …. ……. 230000Additional Paid in Capital-Common Stock.. 233000 . . . . ||| . . . . Mortgage Loan …. …. …. …. …. …… 114000Auditors Fee …. …. …. …. …. …. ….. ….. ….. .. 207000 . . . . ||| . . . . Rent Revenue …. …. …. …. …. …. … 53000Buildings…. …. …. …. …. …. ….. ….. ….. ….. ... 401000 . . . . ||| . . . . Retained Earnings …. …. …. …. …… 52600Cash …. …. …. …. …. …. ….. ….. ….. ….. ….. …. 204340 . . . . ||| . . . . Salaries and Wages Expense …. …. 106000Common Stock ($2 each)…. …. …. …. …. ….. 113000 . . . . ||| . . . . Sales …. …. …. …. …. …. ….. ….. …….…arrow_forwardWildhorse Co. issued $6,720,000 of 8% bonds on October 1, 2020, due on October 1, 2025. The interest is to be paid twice a year on April 1 and October 1. The bonds were sold to yield 10% effective annual interest. Wildhorse Co. closes its books annually on December 31.arrow_forward

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning,

AccountingAccountingISBN:9781337272094Author:WARREN, Carl S., Reeve, James M., Duchac, Jonathan E.Publisher:Cengage Learning, Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning,

Accounting Information SystemsAccountingISBN:9781337619202Author:Hall, James A.Publisher:Cengage Learning, Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON

Horngren's Cost Accounting: A Managerial Emphasis...AccountingISBN:9780134475585Author:Srikant M. Datar, Madhav V. RajanPublisher:PEARSON Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education

Intermediate AccountingAccountingISBN:9781259722660Author:J. David Spiceland, Mark W. Nelson, Wayne M ThomasPublisher:McGraw-Hill Education Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education

Financial and Managerial AccountingAccountingISBN:9781259726705Author:John J Wild, Ken W. Shaw, Barbara Chiappetta Fundamental Accounting PrinciplesPublisher:McGraw-Hill Education