Concept explainers

Videos

Comprehensive Problem 1

✓ 8 Net income. $31,425

Kelly Pitney began her consulting business. Kelly Consulting, on April 1, 20Y8. The accounting cycle for Kelly Consulting for April, including financial statements, was illustrated in this chapter During May, Kelly Consulting entered into the following transactions:

May 3. Received cash from clients as an advance payment for services to be provided and recorded it as unearned tree $4,500

- 5. Received cash from clients on account $2,450.

- 9. Paid cash for a newspaper advertisement $225.

- 13. Raid Office Station Co for part of the debt incurred on April $, $640.

- 15. Recorded services provided on account for the period May 1-15, $9,180.

- 16 Paid part-time receptionist for two weeks’ salary including the amount owed on April 30, $750.

- 17. Recorded cash from cash clients for fees earned during the period May 1–16, $8,360. Record the following transactions on Page 6 of the Journal

- 20. Purchased support on account $735.

- 21. Recorded services provided on account for the period May 16–20. $4,820

- 25. Recorded cash from cash clients for fees earned for the period May 17–23, $7,900

- 27. Received cash from clients on account $9,520.

- 28. Paid part-time receptionist for two weeks’ salary. $7S0.

- 30. Raid telephone bill for May. $260

- 31. Paid electricity bill for May, $810.

- 31. Recorded cash from cash clients tor lees earned for the period May 20–31. $3,300.

- 31. Recorded services provided on account for the remainder of May, $2,650.

- 31. Paid dividends $10,500

Instructions

- 1. The chart of accounts foe Kelly Consulting is shown us Exhibit 9. and the post-closing

trial balance as of April 30, 20Y8, is shown in Exhibit 17. for each account in the post-closing trial balance, enter the balance in the appropriate Balance column of a four-column account. Date the balances May 1. 20Y8. and place a check mark (✓) in the Posting Reference column. Journalize each of the May transactions in a two-column journal starting cm Page $ of the journal and using Kelly Consulting’s chart of accounts. (Do not insert the account numbers in the journal at this time.) - 2. Post the journal to a ledger of four-column accounts.

- 5. Prepare an unadjusted trial balance.

- 4. At the end of May, the following adjustment data were assembled. Analyze and use these data to complete parts (5) and (6).

- (a) Insurance expired during May is $275.

- (b) Supplies on hand on May II are $715.

- (c)

Depreciation of office equipment for May is $330. - (d) Accrued receptionist salary on May 31 is $325.

- (e) Rent expired during May is $1600.

- (f) Unearned fees on May 31 are $3,210

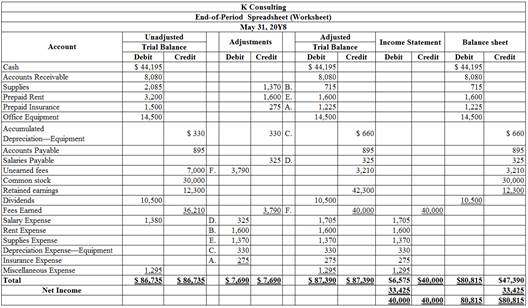

- 5. (Optional) Enter the unadjusted trial balance on an end-of-period spreadsheet and complete the spreadsheet

- 6. Journalize and post the

adjusting entries . Record the adjusting entries on Page 7 of the journal. - 7. Prepare an adjusted trial balance.

- 8. Prepare an income statement, a statement of

stockholders equity , and abalance sheet . - 9. Prepare and post the closing entries. Record the closing entries on Page 8 of the journal. Indicate closed accounts by inserting a line in both the Balance columns opposite the closing entry.

- 10. Prepare a post-closing trial balance.

1.

Journal:

Journal is the book of original entry. Journal consists of the day-to-day financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

To journalize: The transactions of May in a two column journal beginning on page 5.

Explanation of Solution

Journalize the transactions of May in a two column journal beginning on page 5.

| Journal Page 5 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 3 | Cash | 11 | 4,500 | |

| May | Unearned fees | 23 | 4,500 | ||

| (To record the cash received for the service yet to be provide) | |||||

| 5 | Cash | 11 | 2,450 | ||

| Accounts receivable | 12 | 2,450 | |||

| (To record the cash received from clients) | |||||

| 9 | Miscellaneousexpense | 59 | 225 | ||

| Cash | 11 | 225 | |||

| (To record the payment made for Miscellaneous expense) | |||||

| 13 | Accounts payable | 21 | 640 | ||

| Cash | 11 | 640 | |||

| (To record the payment made to creditors on account) | |||||

| 15 | Accounts receivable | 12 | 9,180 | ||

| Fees earned | 41 | 9,180 | |||

| (To record the revenue earned and billed) | |||||

| 14 | Salary Expense | 51 | 630 | ||

| Salaries payable | 22 | 120 | |||

| Cash | 11 | 750 | |||

| (To record the payment made for salary) | |||||

| Cash | 11 | 8,360 | |||

| 17 | Fees earned | 41 | 8,360 | ||

| (To record the receipt of cash) | |||||

Table (1)

| Journal Page 6 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 18 | Supplies | 14 | 735 | |

| May | Accounts payable | 21 | 735 | ||

| (To record the payment made for automobile expense) | |||||

| 21 | Accounts receivable | 12 | 4,820 | ||

| Fees earned | 41 | 4,820 | |||

| (To record the payment of advertising expense) | |||||

| 25 | Cash | 11 | 7,900 | ||

| Fees earned | 41 | 7,900 | |||

| (To record the cash received from client for fees earned) | |||||

| 27 | Cash | 11 | 9,520 | ||

| Accounts receivable | 12 | 9,520 | |||

| (To record the cash received from clients) | |||||

| 28 | Salary expense | 51 | 750 | ||

| Cash | 11 | 750 | |||

| (To record the payment of salary) | |||||

| 30 | Miscellaneous Expense | 59 | 260 | ||

| Cash | 11 | 260 | |||

| (To record the payment of telephone charges) | |||||

| 31 | Miscellaneous Expense | 59 | 810 | ||

| Cash | 11 | 810 | |||

| (To record the payment of electricity charges) | |||||

| 31 | Cash | 11 | 3,300 | ||

| Fees earned | 41 | 3,300 | |||

| (To record the cash received from client for fees earned) | |||||

| 31 | Accounts receivable | 12 | 2,650 | ||

| Fees earned | 41 | 2,650 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Dividends | 33 | 10,500 | ||

| Cash | 11 | 10,500 | |||

| (To record the drawing made for personal use) | |||||

Table (2)

(2), (6) and (9)

To record: The balance of each accounts in the appropriate balance column of a four-column account and post them to the ledger.

Explanation of Solution

T-Accounts:

T-accounts are referred as T-account because its format represents the letter “T”. The T-accounts consists of the following:

- The title of accounts.

- The debit side (Dr.) and,

- The credit side (Cr).

| Account: Cash Account no.11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 22,100 | |||

| 3 | 5 | 4,500 | 26,600 | ||||

| 5 | 5 | 2,450 | 29,050 | ||||

| 9 | 5 | 225 | 28,825 | ||||

| 13 | 5 | 640 | 28,185 | ||||

| 16 | 5 | 750 | 27,435 | ||||

| 17 | 5 | 8,360 | 35,795 | ||||

| 25 | 6 | 7,900 | 43,695 | ||||

| 27 | 6 | 9,520 | 53,215 | ||||

| 28 | 6 | 750 | 52,465 | ||||

| 30 | 6 | 260 | 52,205 | ||||

| 31 | 6 | 810 | 51,395 | ||||

| 31 | 6 | 3,300 | 54,695 | ||||

| 31 | 6 | 10,500 | 44,195 | ||||

Table (3)

| Account: Accounts ReceivableAccount no.12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 3,400 | |||

| 5 | 5 | 2,450 | 950 | ||||

| 15 | 5 | 9,180 | 10,130 | ||||

| 21 | 6 | 4,820 | 14,950 | ||||

| 27 | 6 | 9,520 | 5,430 | ||||

| 31 | 6 | 2,650 | 8,080 | ||||

Table (4)

| Account: SuppliesAccount no.14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 1,350 | |||

| 20 | 6 | 735 | 2,085 | ||||

| 30 | Adjusting | 7 | 1,350 | 715 | |||

Table (5)

| Account: Prepaid RentAccount no.15 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 3,200 | |||

| 31 | Adjusting | 7 | 1,600 | 1,600 | |||

Table (6)

| Account: Prepaid InsuranceAccount no.16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 1,500 | |||

| 31 | Adjusting | 7 | 275 | 1,225 | |||

Table (7)

| Account: Office equipmentAccount no.18 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 14,500 | |||

Table (8)

| Account: Accumulated Depreciation-Office equipmentAccount no.19 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 330 | |||

| 31 | Adjusting | 7 | 330 | 660 | |||

Table (9)

| Account: Accounts Payable Account no.21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 800 | |||

| 13 | 5 | 640 | 160 | ||||

| 20 | 6 | 735 | 895 | ||||

Table (10)

| Account: Salaries Payable Account no.22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 120 | |||

| 16 | 5 | 120 | |||||

| 31 | Adjusting | 7 | 325 | 325 | |||

Table (11)

| Account: Unearned Fees Account no.23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 2,500 | |||

| 3 | 5 | 4,500 | 7,000 | ||||

| 31 | Adjusting | 7 | 3,790 | 3,210 | |||

Table (12)

| Account: Common StockAccount no.31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 30,000 | |||

Table (13)

| Account: Retained EarningsAccount no.32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 1 | Balance | ✓ | 12,300 | |||

| 31 | Closing | 8 | 33,425 | 45,725 | |||

| 31 | Closing | 8 | 10,500 | 35,225 | |||

Table (14)

| Account: DividendsAccount no.33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | 6 | 10,500 | 10,500 | |||

| 31 | Closing | 8 | 10,500 | ||||

Table (15)

| Account: Income SummaryAccount no.34 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Closing | 8 | 40,000 | 40,000 | ||

| 31 | Closing | 8 | 6,575 | 33,425 | |||

| 31 | Closing | 8 | 33,425 | ||||

Table (16)

| Account: Fees earned Account no.41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 15 | 5 | 9,180 | 9,180 | |||

| 17 | 5 | 8,360 | 17,540 | ||||

| 21 | 6 | 4,820 | 22,360 | ||||

| 25 | 6 | 7,900 | 30,260 | ||||

| 31 | 6 | 3,300 | 33,560 | ||||

| 31 | 6 | 2,650 | 36,210 | ||||

| 31 | Adjusting | 7 | 3,790 | 40,000 | |||

| 31 | Closing | 8 | 40,000 | ||||

Table (17)

| Account: Salary expense Account no.51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 16 | 5 | 630 | 630 | |||

| 28 | 6 | 750 | 1,380 | ||||

| 31 | Adjusting | 7 | 325 | 1,705 | |||

| 31 | Closing | 8 | 1,705 | ||||

Table (18)

| Account: Rent expense Account no.52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 1,600 | 1,600 | ||

| 31 | Closing | 8 | 1,600 | ||||

Table (19)

| Account: Supplies expense Account no.53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 1,370 | 1,370 | ||

| 31 | Closing | 8 | 1,370 | ||||

Table (20)

| Account: Depreciation expense Account no.54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 330 | 330 | ||

| 31 | Closing | 8 | 330 | ||||

Table (21)

| Account: Insurance expense Account no.54 | |||||||

| Date | Item | PostRef. |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 31 | Adjusting | 7 | 275 | 275 | ||

| 31 | Closing | 8 | 275 | ||||

Table (22)

| Account: Miscellaneous expense Account no.59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| May | 9 | 5 | 225 | 225 | |||

| 30 | 6 | 260 | 485 | ||||

| 31 | 6 | 810 | 1,295 | ||||

| 31 | Closing | 8 | 1,295 | ||||

Table (23)

(3)

To prepare: The unadjusted trial balance of Consulting Kat May, 31.

Explanation of Solution

Adjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of Consulting K for the month ended May, 31 as follows:

|

K Consulting Unadjusted Trial Balance May 31, 20Y8 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 2,085 | |

| Prepaid rent | 15 | 3,200 | |

| Prepaid insurance | 16 | 1,500 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation-Office equipment | 19 | 330 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 0 | |

| Unearned fees | 23 | 7,000 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 36,210 | |

| Salary expense | 51 | 1,380 | |

| Rent expense | 52 | 0 | |

| Supplies expense | 53 | 0 | |

| Depreciation expense | 54 | 0 | |

| Insurance expense | 55 | 0 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 86,735 | 86,735 | |

Table (22)

The debit column and credit column of the unadjusted trial balance are agreed, both having balance of $86,735.

(5)

To enter: The unadjusted trial balance on an end-of-period spreadsheet.

Explanation of Solution

The unadjusted trial balance on an end-of-period spreadsheet is prepared as follows:

Table (23)

Hence, the unadjusted trial balance on an end-of-period spreadsheet is prepared and completed.

(6)

To Journalize: The adjusting entries of Consulting K for May 31.

Explanation of Solution

Adjusting entries:

An adjusting entry is prepared when the trial balance is not up-to-date, and complete, and they are usually prepared at the end of the accounting period. This adjusting entry is essential for preparing the financial statements of the business.

The adjusting entries of ConsultingK for May 31, 20Y8are as follows:

| Date | Accounts title and explanation | Post Ref. |

Debit ($) |

Credit ($) |

|

| 20Y8 | Insurance expense | 55 | 275 | ||

| May | 31 | Prepaid insurance | 16 | 275 | |

| (To record the insurance expense for May ) | |||||

| 31 | Supplies expense(1) | 53 | 1,370 | ||

| Supplies | 14 | 1,370 | |||

| (To record the supplies expense) | |||||

| 31 | Depreciation expense | 54 | 330 | ||

| Accumulated Depreciation | 19 | 330 | |||

| (To record the depreciation and the accumulated depreciation) | |||||

| 31 | Salaries expense | 51 | 325 | ||

| Salaries payable | 22 | 325 | |||

| (To record the accrued salaries payable) | |||||

| 31 | Rent expense | 52 | 1,600 | ||

| Prepaid rent | 15 | 1,600 | |||

| (To record the rent expense for May ) | |||||

| 31 | Unearned fees(2) | 23 | 3,790 | ||

| Fees earned | 41 | 3,790 | |||

| (To record the receipt of unearned fees) | |||||

Table (24)

Working notes:

(7)

To prepare: An adjusted trial balance of Consulting K for May 31, 20Y8.

Explanation of Solution

Spreadsheet: A spreadsheet is a worksheet. It is used while preparing a financial statement. It is a type of form having multiple columns and it is used in the adjustment process. The use of a worksheet is optional for any organization. A worksheet can neither be considered as a journal nor a part of the general ledger.

An adjusted trial balanceof Consulting K for May 31, 20Y8 is prepared as follows:

|

K Consulting Adjusted Trial Balance May 31, 20Y8 |

|||

| Particulars |

Account No. |

Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid insurance | 16 | 1,600 | |

| Prepaid rent | 15 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated Depreciation-Office equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned fees | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 12,300 | |

| Dividends | 33 | 10,500 | |

| Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | |

| Rent expense | 52 | 1,600 | |

| Supplies Expense | 53 | 1,370 | |

| Depreciation expense | 54 | 330 | |

| Insurance expense | 55 | 275 | |

| Miscellaneous expense | 59 | 1,295 | |

| Total | 87,390 | 87,390 | |

Table (25)

The debit column and credit column of the adjusted trial balance are agreed, both having balance of $87,390.

(8)

To Prepare: An income statement for the year ended May 31, 20Y8.

Explanation of Solution

Income statement:

An income statement is one of the financial statements which shows the revenues, and expenses of the company. The income statement is prepared to ascertain the net income/loss of the company, by deducting the expenses from the revenues.

An income statement for the year ended May 31, 20Y8 is as follows:

| K Consulting | ||

| Income Statement | ||

| For the year ended May 31, 20Y8 | ||

| Particulars | Amount ($) | Amount ($) |

| Revenues: | ||

| Fees Earned | 40,000 | |

| Expenses: | ||

| Salaries Expense | 1,705 | |

| Rent Expense | 1,600 | |

| Supplies Expense | 1,370 | |

| Depreciation Expense- Building | 330 | |

| Insurance Expense | 275 | |

| Miscellaneous Expense | 1,295 | |

| Total Expenses | 6,575 | |

| Net Income | $33,425 | |

Table (26)

Hence, the net income of K Consultingfor the year ended May 31, 20Y8is $33,425.

To Prepare: The statement of stockholders’ equity for the year ended May 31, 20Y8.

Explanation of Solution

The statement of stockholders’ equity for the year ended May 31, 20Y8 is as follows:

| G Consulting | ||

| Statement of Stockholders’ Equity | ||

| For the Year Ended May 31, 20Y8 | ||

| Particulars | Amount ($) | Amount ($) |

| Balance, May 1, 20Y7 | 12,300 | |

| Add: Net income | 33,425 | |

| Less: Dividends | (10,500) | |

| Change in retained earnings | 22,925 | |

| Balance, May 31, 20Y8 | $35,225 | |

Table (27)

Hence, retained earnings for the year ended May 31, 20Y8is $35,225.

To Prepare: The balance sheet of K Consulting at May 31, 20Y8.

Answer to Problem 1COP

Balance sheet:

A balance sheet is a financial statement consists of the assets, liabilities, and the stockholder’s equity of the company. The balance of the assets account must be equal to that of the liabilities and the stockholder’s equity account.

| K Consulting | |||

| Balance Sheet | |||

| May 31, 20Y8 | |||

| Assets | |||

| Current Assets: | $ | $ | |

| Cash | 44,195 | ||

| Accounts Receivable | 8,080 | ||

| Supplies | 715 | ||

| Prepaid Rent | 1,600 | ||

| Prepaid Insurance | 1,225 | ||

| Total Current Assets | 55,815 | ||

| Property, plant and equipment: | |||

| Office Equipment | 14,500 | ||

| Less: Accumulated Depreciation | (660) | ||

| Total Plant Assets | 13,840 | ||

| Total Assets | $69,655 | ||

| Liabilities | |||

| Current Liabilities: | |||

| Accounts Payable | 895 | ||

| Salaries Payable | 325 | ||

| Unearned rent | 3,210 | ||

| Total Liabilities | $4,430 | ||

| Stockholder’s Equity | |||

| Common stock | 30,000 | ||

| Retained earnings | 35,225 | ||

| Total stockholder’s equity | 65,225 | ||

| Total Liabilities and stockholder’s Equity | $69,655 | ||

Table (28)

Explanation of Solution

It is one of the financial statements, which shows the assets, liabilities, and stockholders’ equity of a company at a particular point of time. It reveals the financial health of a company. Thus, this statement is also called as the Statement of Financial Position. It helps the users to know about the creditworthiness of a company as to whether the company has enough assets to pay off its liabilities.

Therefore, the total assets and total liabilities plus owners’ equity of Consulting Kat May 31, 20Y8 is $69,655.

(9)

To Journalize: The closing entries for KConsulting.

Answer to Problem 1COP

Closing entry for revenue and expense accounts:

| Date | Accounts title and Explanation | Post Ref. |

Debit ($) |

Credit ($) |

| May 31, 20Y8 | Fees earned | 41 | 40,000 | |

| Salary expense | 51 | 1,705 | ||

| Rent Expense | 52 | 1,600 | ||

| Supplies Expense | 53 | 1,370 | ||

| Depreciation Expense | 54 | 330 | ||

| Insurance Expense | 55 | 275 | ||

| Miscellaneous Expense | 59 | 1,295 | ||

| Retained earnings | 34 | 33,425 | ||

| (To close the revenues and expenses account. Then the balance amount are transferred to retained earnings account) | ||||

| May 31, 20Y8 | Retained earnings | 32 | 10,500 | |

| Dividends | 33 | 10,500 | ||

| (To close the dividend account to retained earnings account) |

Table (4)

Explanation of Solution

Closing entries

Closing entries are recorded in order to close the temporary accounts such as incomes and expenses by transferring them to the permanent accounts such as retained earnings. It is passed at the end of the accounting period, to transfer the final balance.

Process of closing:

- The balance of revenue and expense are transferred to retrained earnings account.

- The balance of dividend account is transferred to retained earnings account to close the temporary accounts.

Rules of Debit and Credit:

- Debit, the revenue account and retained earnings account balance. In addition debit retained earnings account if it suffer loss (net loss)

- Credit, the expense account, retained earnings if it earn income (net income) and dividend account.

- Fees earned are a revenue account. Since the amount of revenue is closed and transferred to retained earnings account. Here, AS Company earned an income of $33,425. Therefore, it is debited.

- Wages Expense, Rent Expense, Insurance Expense, Utilities Expese, Supplies Expense, Depreciation Expense and Miscellaneous Expense are expense accounts. Since the amount of expenses are closed to Income Summary account. Therefore, it is credited.

Working Note:

Calculate net income on income summary account:

- The Dividend is paid to the shareholders out of the Retained Earnings. Thus, Retained Earnings is debited since the earnings are decreased on payment of dividend.

- Dividends is a component of stockholders’ equity account. It is credited because dividends are transferred to Retained Earnings account.

(10)

To Journalize: The closing entries for KConsulting.

Explanation of Solution

Post-Closing Trial Balance:

After passing all the journal entries and the closing entries of the permanent accounts and then further posting them to each of the respective accounts, a post-closing trial balance is prepared which consists of a list of all the permanent accounts. A post-closing trial balance serves as an evidence to prove that the balance of the permanent accounts is equal.

Prepare apost–closing trial balance of KConsulting for the month ended May 31, 20Y8 as follows:

|

Consulting K Post-closing Trial Balance May, 31, 20Y8 |

|||

| Particulars | Account Number | Debit $ | Credit $ |

| Cash | 11 | 44,195 | |

| Accounts receivable | 12 | 8,080 | |

| Supplies | 14 | 715 | |

| Prepaid rent | 15 | 1,600 | |

| Prepaid insurance | 16 | 1,225 | |

| Office Equipment | 18 | 14,500 | |

| Accumulated depreciation –Office Equipment | 19 | 660 | |

| Accounts payable | 21 | 895 | |

| Salaries payable | 22 | 325 | |

| Unearned rent | 23 | 3,210 | |

| Common stock | 31 | 30,000 | |

| Retained earnings | 32 | 35,225 | |

| Total | 70,315 | 70,315 | |

Table (5)

The debit column and credit column of the post–closing trial balance are agreed, both having balance of $70,315

Want to see more full solutions like this?

Chapter 4 Solutions

Cengagenowv2, 1 Term Printed Access Card For Warren/jones’ Corporate Financial Accounting, 15th

- FINANCIAL RATIOS Use the work sheet and financial statements prepared in Problem 15-8B. All sales are credit sales. The Accounts Receivable balance on January 1 was 38,200. REQUIRED Prepare the following financial ratios: (a)Working capital (b)Current ratio (c)Quick ratio (d)Return on owners equity (e)Accounts receivable turnover and the average number of days required to collect receivables (f)Inventory turnover and the average number of days required to sell inventoryarrow_forwardconstruct the Journal Entry of the transaction: Date/# Account Title Debit Credit Oct-01 Garcia invested P30,000 cash to start his business. 2 Purchased medical Supplies on account, P10,000 2 Paid monthly office rent of P4,000. 3 Recorded P5,000 revenue for service rendered to patients: received cash of P2,000 and sent bills to patients for the remainder. 15 Borrowed P50,000 from the bank, signing a note payable 22 Performed service for patients on account, P3,600 30 Received cash from patients billed on September 3, P2,000 31 Received and paid a utility bill, P200 31 Paid monthly salary to nurses, P3,000 31 Paid interest expense of P200arrow_forwardParts wriiten Subparts to be solve are the ones to be solved Question Requirement 1For each of the following transactions make the required entries in the General Journal:(See the General Ledger tab in the workbook Chapter 03 b - Problem 3-1 Forms for the accounts in OPJ’s accounting system.)Feb 01 Take $4,000 cash out of Big Bank to pay for February’s warehouse rent.Feb 04 Sale of inventory to a customer – selling price $62,000 – cost of inventory sold $16,000 – customer paid cash which was deposited in Big Bank.Feb 07 Take $10,000 cash out of Little Bank to pay employees for wages they have earned.Feb 15 Sale of inventory to a customer – selling price $88,000 – cost of inventory sold $22,000 – customer will pay in the future.Feb 18 Sale of inventory to a customer – selling price $110,000 – cost of inventory sold $28,000 – customer pays $40,000 cash which is deposited in Little Bank – customer will pay for the remaining amount of the sale in 30 days.Feb 22 Purchase additional…arrow_forward

- QUESTION 1 a) You are the accounts executive for BFC Enterprise. You are responsible to prepare the monthly receivables and payables control accounts for the business. Following are balances from the company’s record at 1 February 2020. Dr RM Cr RM Debtor ledger control account 54,000 1,000 Creditor ledger control account 200 43,000 The following information is extracted in February 2020 from the company’s records: RM Credit sales 251,000 Cash sales 34,000 Credit purchases…arrow_forwardRequirement 1 For each of the following transactions make the required entries in the General Journal: (See the General Ledger tab in the workbook Chapter 03 b - Problem 3-1 Forms for the accounts in OPJ’s accounting system.) Feb 01 Take $4,000 cash out of Big Bank to pay for February’s warehouse rent. Feb 04 Sale of inventory to a customer – selling price $62,000 – cost of inventory sold $16,000 – customer paid cash which was deposited in Big Bank. Feb 07 Take $10,000 cash out of Little Bank to pay employees for wages they have earned. Feb 15 Sale of inventory to a customer – selling price $88,000 – cost of inventory sold $22,000 – customer will pay in the future. Feb 18 Sale of inventory to a customer – selling price $110,000 – cost of inventory sold $28,000 – customer pays $40,000 cash which is deposited in Little Bank – customer will pay for the remaining amount of the sale in 30 days. Feb 22 Purchase additional inventory – pay $17,000 cash out of Big Bank for the inventory. Feb 27…arrow_forwardrrent Attempt in Progress n providing accounting services to small businesses, you encounter the following situations. 1. 2. Lily Corporation rings up cash sales and sales taxes separately on its cash register. On April 10, the register totals are pre-tax sales of sales $4,200 plus GST of $210 and PST of $336. (i) During the month of March, Bramble Corporation's employees earned gross salaries of $60,000. Withholdings deducted from employee earnings related to these salaries were $3,254 for CPP, $948 for El, $7,050 for income taxes. (ii) Bramble's employer portions were $3,254 for CPP and $1,327 for El for the month. Prepare the journal entries to record the above transactions. (Credit account titles are automatically indented when the amount is entered. Do not indent manually. If no entry is required, select "No Entry" for the account titles and enter O for the amounts. List all debit entries before credit entries.)arrow_forward

- Notes Receivable Crowne Cleaning provides cleaning services for Amber Inc., a business with four buildings. Crowne assigned different cleaning charges for each building based on the amount of square feet to be cleaned. The charges for the four buildings are $87,600, $82,200, $102,000, and $62,400. Amber secured this amount by signing a note bearing 10% interest on June 1. Required: Question Content Area 1. Prepare the journal entry to record the sale on June 1. If an amount box does not require an entry, leave it blank. blank - Select - - Select - - Select - - Select - Question Content Area 2. Determine how much interest Crowne will receive if the note is repaid on December 1.$fill in the blank 59d6dd028fbe01b_1 Question Content Area 3. Prepare Crowne’s journal entry to record the cash received to pay off the note and interest on December 1. If an amount box does not require an entry, leave it blank. blank - Select - - Select…arrow_forwardSession Timed Out 9 Chapter 12: Payroll Accounting A ezto.mheducation.com/hm.tpx E Apps O Harford County Pu. start.hcps.org aSummary- Quizizz a Summary - Quizizz 9 Geometry Unit 3 St.. I connect Accounting & Finance: B4 JACCOUNTING Chapter 12: Payroll Accounting Question 1 (of 12) 1. The sales clerks of Teresa's Treasures are paid a sales they make. Find the amount of commission and gross earnings for these employees. (Round your answers to 2 decimal places. Omit the "$" sign in your response.) lary of $225 per ek plus a commission 8% on all Sales for the Week Name Commission Gross Earnings S 2,392.50 $ 3,480.75 Tina Valendez Jan Yarrow 02021 McGraw-Hill Education. ll rights P Search for anything DELLarrow_forwardTB 03-70 Company A receives $10,000 in advance this m... Company A receives $10,000 in advance this month for work to be performed next month. This month, the company should: Multiple Choice Debit Accounts Payable $10,000 and credit Cash $10,00. Debit Inventory $10,000 and credit Sales Revenue $10,000. Debit Cash $10,000 and credit Deferred Revenue $10,000. Debit Inventory $10,000 and credit Accounts Payable $10,000.arrow_forward

- Question 1 Catherine’s Cookies has a beginning balance in the Accounts Payable control total account of RO 8,200. In the cash disbursements journal, the Accounts Payable column has total debits of RO 6,800 for November. The Accounts Payable credit column in the purchases journal reveals a total of RO10,500 for the current month. Based on this information, what is the ending balance in the Accounts Payable account in the general ledger? Question 2 Record the following transactions in the cash receipts journal. Jun. 12 Your company received payment in full from Jolie Inc. in the amount of RO1,225 for merchandise purchased on June 4 for RO1,250, invoice number No.1032. Jolie Inc. was offered terms of 2/10, n/30. Record the payment. Jun. 15 Portman Inc. mailed you a check for RO2500. The company paid for invoice No.1027, dated June 1, in the amount of RO2,500, terms offered 3/10, n/30. Jun. 17 Your company received a refund check (its check No.12440) from the State…arrow_forwardAdriana Graphic Design receives $2,250 from a client billed in a previous month for services provided. Which of the following general journal entries will Adriana Graphic Design make to record this transaction? Multiple Choice Cash 2,250 Accounts Receivable 2,250 Cash 2,250 Unearned Design Revenue 2,250 Accounts Receivable 2,250 Unearned Design Revenue 2,250 Prev 3 of 10 Next > nere to search W P 99% 9:34 PM 2/21/2022arrow_forwardKnowledge Check 01 On December 31, the company provides consulting services and bills its customer $3,000 for these services. Complete the necessary journal entry by selecting the account names from the pull-down menus and entering dollar amounts in the debit and credit columns. View transaction list Journal entry worksheet 1 > On December 31, the company provides consulting services and bills its customer $3,000 for these services. Note: Enter debits before credits. %24 ... *.*.......... 6:1 3/27/ Insert Prt Sc F3 F4 F5 F6 EZ F8 F9 F10 F11 F12 Fn Lockarrow_forward

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage LearningCentury 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:Cengage Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,

Financial And Managerial AccountingAccountingISBN:9781337902663Author:WARREN, Carl S.Publisher:Cengage Learning,