Concept explainers

Videos

Journal entries and

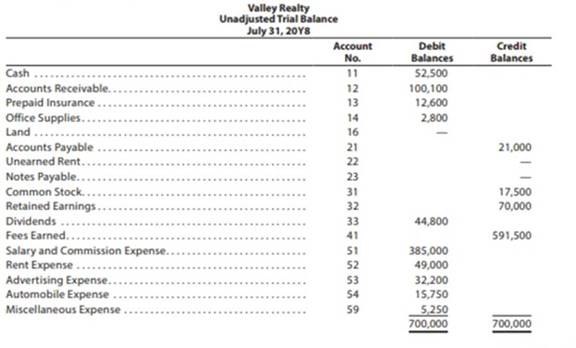

Valley Realty acts as an agent in buying, selling, renting, and managing real estate. The unadjusted trial balance on July 31, 20Y8, follows:

The following I hi sine vs transactions were completed by Valley Realty during August 20Y8:

Aug. 1. Purchased office supplies on account, $3,150.

2. Paid rent on office for month, $7,200.

3. Received cash from clients on account, $83,900.

5. Paid insurance premiums, $ 12.000.

9. Returned a portion of the office supplies purchased on August 1, receiving full credit for their cost, $400.

17. Paid advertising expense, $8,000.

23. Paid creditors on account, $ 13,750.

Enter the following transactions on Page 19 of the two-column journal:

29. Paid miscellaneous expenses, $ 1,700.

30. Paid automobile expense (including rental charges for an automobile), $2,500.

31. Discovered an error in computing a commission during Ally; received cash from the salesperson for the overpayment, $2,000.

31. Paid salaries and commissions for the month, $53,000.

31. Recorded revenue earned and billed to clients during the month, $183,500.

31. Purchased land for a future building site for $75,000, paying $7,500 in cash and giving a note payable for the remainder.

31. Paid dividends, $1,000.

31. Rented land purchased on August 31 to a local university for use as a parking lot during football season (September. October, and November); received advance payment of $5,000.

Instructions

1. Record the August 1 balance of each account in the appropriate balance column of a four-column account, write Balance in item section, and place a check mark (»O in the Posting Reference column.

2. Journalize the transactions for August in a two-column journal beginning on Page 18.

3. Post to the ledger, extending the account balance to the appropriate balance column after each posting.

4. Prepare an unadjusted trial balance of the ledger as of August 31. 20Y8.

5. Assume that the August 31 transaction for dividends should have been $10,000. (a) Why did the unadjusted trial balance in (4) balance? (b) Journalize the correcting entry, (c) Is this error a transposition or slide?

(2) and (3)

To journalize: The transactions of August in a two column journal beginning on page 18.

Explanation of Solution

Journal:

Journal is the book of original entry. Journal consists of the day today financial transactions in a chronological order. The journal has two aspects; they are debit aspect and the credit aspect.

Rules of debit and credit:

“An increase in an asset account, an increase in an expense account, a decrease in liability account, and a decrease in a revenue account should be debited.

Similarly, an increase in liability account, an increase in a revenue account and a decrease in an asset account, a decrease in an expenses account should be credited”.

Journalize the transactions of August in a two column journal beginning on page 18.

| Journal Page 18 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | Office supplies | 14 | 3,150 | ||

| August | 1 | Accounts payable | 21 | 3,150 | |

| (To record the purchase of supplies of account) | |||||

| 2. | Rent expense | 52 | 7,200 | ||

| Cash | 11 | 7,200 | |||

| (To record the payment of rent) | |||||

| 3 | Cash | 11 | 83,900 | ||

| Accounts receivable | 12 | 83,900 | |||

| (To record the receipt of cash from clients) | |||||

| 5 | Prepaid insurance | 13 | 12,000 | ||

| Cash | 11 | 12,000 | |||

| (To record the payment of insurance premium) | |||||

| 9 | Accounts payable | 21 | 400 | ||

| Office supplies | 14 | 400 | |||

| (To record the payment made to creditors on account) | |||||

| 17 | Advertising expense | 53 | 8,000 | ||

| Cash | 11 | 8,000 | |||

| (To record the payment of advertising expense) | |||||

| 23 | Accounts payable | 21 | 13,750 | ||

| Cash | 11 | 13,750 | |||

| (To record the payment made to creditors on account) | |||||

Table (1)

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | 29 | Miscellaneous expense | 59 | 1,700 | |

| August | Cash | 11 | 1,700 | ||

| (To record the payment made for Miscellaneous expense) | |||||

| 30 | Automobile expense | 54 | 2,500 | ||

| Cash | 11 | 2,500 | |||

| (To record the payment made for automobile expense) | |||||

| 31 | Cash | 11 | 2,000 | ||

| Salary and commission expense | 51 | 2,000 | |||

| (To record the receipt of cash) | |||||

| 31 | Salary and commission expense | 51 | 53,000 | ||

| Cash | 11 | 53,000 | |||

| (To record the payment made for salary and commission expense) | |||||

| 31 | Accounts receivable | 12 | 183,500 | ||

| Fees earned | 41 | 183,500 | |||

| (To record the revenue earned and billed) | |||||

| 31 | Land | 16 | 75,000 | ||

| Cash | 11 | 7,500 | |||

| Notes payable | 23 | 67,500 | |||

| (To record the purchase of land party for cash and party on signing a note) | |||||

| 31 | Dividends | 33 | 1,000 | ||

| Cash | 11 | 1,000 | |||

| (To record the drawing made for personal use) | |||||

| 31 | Cash | 11 | 5,000 | ||

| Unearned rent | 22 | 5,000 | |||

| (To record the cash received for the service yet to be provide) | |||||

Table (2)

(1) and (3)

To record: The beginning balances of each accounts in the appropriate balance column of a four-column account, and post them to the ledger extending the account balance to the appropriate balance column after each posting.

Explanation of Solution

T-account:

An account is referred to as a T-account, because the alignment of the components of the account resembles the capital letter ‘T’. An account consists of the three main components which are as follows:

- The title of the account

- The left or debit side

- The right or credit side

| Account: Cash Account no. 11 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 52,500 | |||

| 2 | 18 | 7,200 | 45,300 | ||||

| 3 | 18 | 83,900 | 129,200 | ||||

| 5 | 18 | 12,000 | 117,200 | ||||

| 17 | 18 | 8,000 | 109,200 | ||||

| 23 | 18 | 13,750 | 95,450 | ||||

| 29 | 19 | 1,700 | 93,750 | ||||

| 30 | 19 | 2,500 | 91,250 | ||||

| 31 | 19 | 2,000 | 93,250 | ||||

| 31 | 19 | 53,000 | 40,250 | ||||

| 31 | 19 | 7,500 | 32,750 | ||||

| 31 | 19 | 1,000 | 31,750 | ||||

| 31 | 19 | 5,000 | 36,750 | ||||

Table (3)

| Account: Accounts Receivable Account no. 12 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 100,100 | |||

| 3 | 18 | 83,900 | 16,200 | ||||

| 31 | 19 | 183,500 | 199,700 | ||||

Table (4)

| Account: Prepaid Insurance Account no. 13 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 12,600 | |||

| 5 | 18 | 12,000 | 24,600 | ||||

Table (5)

| Account: Office Supplies Account no. 14 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 2,800 | |||

| 1 | 18 | 3,150 | 5,950 | ||||

| 9 | 18 | 400 | 5,550 | ||||

Table (6)

| Account: Land Account no. 16 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 75,000 | 75,000 | |||

Table (7)

| Account: Accounts Payable Account no. 21 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 21,000 | |||

| 1 | 18 | 3,150 | 24,150 | ||||

| 9 | 18 | 400 | 23,750 | ||||

| 23 | 18 | 13,750 | 10,000 | ||||

Table (8)

| Account: Unearned Rent Account no. 22 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 5,000 | 5,000 | |||

Table (9)

| Account: Notes Payable Account no. 23 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 31 | 19 | 67,500 | 67,500 | |||

Table (11)

| Account: Common stock Account no. 31 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 17,500 | |||

Table (12)

| Account: Retained earnings Account no. 32 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 70,000 | |||

Table (13)

| Account: Dividends Account no. 33 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 44,800 | |||

| 31 | 19 | 1,000 | 45,800 | ||||

Table (13)

| Account: Fees earned Account no. 41 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 591,500 | |||

| 31 | 19 | 183,500 | 775,000 | ||||

Table (14)

| Account: Salary and commission expense Account no. 51 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 385,000 | |||

| 31 | 19 | 2,000 | 383,000 | ||||

| 31 | 19 | 53,000 | 436,000 | ||||

Table (15)

| Account: Rent expense Account no. 52 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 49,000 | |||

| 2 | 18 | 7,200 | 56,200 | ||||

Table (16)

| Account: Advertising expense Account no. 53 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 32,200 | |||

| 17 | 18 | 8,000 | 40,200 | ||||

Table (17)

| Account: Automobile expense Account no. 54 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 15,750 | |||

| 30 | 19 | 2,500 | 18,250 | ||||

Table (19)

| Account: Miscellaneous expense Account no. 59 | |||||||

| Date | Item | Post. Ref |

Debit ($) | Credit ($) | Balance | ||

| Debit ($) | Credit ($) | ||||||

| 20Y8 | |||||||

| August | 1 | Balance | ✓ | 5,250 | |||

| 29 | 19 | 1,700 | 6,950 | ||||

Table (20)

(4)

To prepare: An unadjusted trial balance of Company V at August 31, 20Y8.

Explanation of Solution

Unadjusted trial balance:

The unadjusted trial balance is the summary of all the ledger accounts that appears on the ledger accounts before making adjusting journal entries.

Prepare an unadjusted trial balance of Company V at August 31, 20Y8 as follows:

|

Company V Unadjusted Trial Balance August 31, 20Y8 | |||

| Particulars | Account No. |

Debit $ | Credit $ |

| Cash | 11 | 36,750 | |

| Accounts receivable | 12 | 199,700 | |

| Prepaid insurance | 13 | 24,600 | |

| Office supplies | 14 | 5,550 | |

| Land | 16 | 75,000 | |

| Accounts payable | 21 | 10,000 | |

| Unearned rent | 22 | 5,000 | |

| Notes payable | 23 | 67,500 | |

| Common stock | 31 | 17,500 | |

| Retained earnings | 32 | 70,000 | |

| Dividends | 33 | 45,800 | |

| Fees earned | 41 | 775,000 | |

| Salaries and commission expense | 51 | 436,000 | |

| Rent expense | 52 | 56,200 | |

| Advertising expense | 53 | 40,200 | |

| Automobile expense | 54 | 18,250 | |

| Miscellaneous expense | 59 | 6,950 | |

| Total | 945,000 | 945,000 | |

Table (20)

(5) a.

To explain: Whether the unadjusted trial balance in (4) balance

Explanation of Solution

The unadjusted trial balance in (4) would still balance, since the debit equalized the credit in the original journal entry.

b.

To journalize: The correcting entry

Explanation of Solution

The Correcting entry is as follows:

| Journal Page 19 | |||||

| Date | Description | Post. Ref | Debit ($) | Credit ($) | |

| 20Y8 | Dividends | 33 | 9,000 | ||

| August | 31 | Cash | 11 | 9,000 | |

| (To record the correcting entry) | |||||

Table (21)

Working notes:

c.

To identify: Whether the error made is a slide or transposition.

Explanation of Solution

Slide error:

A slide error occurs, when the decimal point of an amount has been misplaced.

The drawings account balance recorded as $10,000 instead of $1,000 is a slide error. Since, the decimal point of the amount has been misplaced.

Want to see more full solutions like this?

Chapter 2 Solutions

CORPORATE FINANCIAL ACCOUNTING 15TH ED

- Prepare journal entries to record the following transactions that occurred in March: A. on first day of the month, purchased building for cash, $75,000 B. on fourth day of month, purchased inventory, on account, $6,875 C. on eleventh day of month, billed customer for services provided, $8,390 D. on nineteenth day of month, paid current month utility bill, $2,000 E. on last day of month, paid suppliers for previous purchases, $2,850arrow_forwardPlumb Line Surveyors provides survey work for construction projects. The office staff use office supplies, while surveying crews use field supplies. Purchases on account completed by Plumb Line Surveyors during May are as follows: Instructions 1. Insert the following balances in the general ledger as of May 1: 2. Insert the following balances in the accounts payable subsidiary ledger as of May 1: 3. Journalize the transactions for May, using a purchases journal (p. 30) similar to the one illustrated in this chapter. Prepare the purchases journal with columns for Accounts Payable, Field Supplies, Office Supplies, and Other Accounts. Post to the creditor accounts in the accounts payable subsidiary ledger immediately after each entry. 4. Post the purchases journal to the accounts in the general ledger. 5. a. What is the sum of the creditor balances in the subsidiary ledger at May 31? b. What is the balance of the accounts payable controlling account at May 31? 6. What type of e-commerce application would be used to plan and coordinate transactions with suppliers?arrow_forwardrowne Cleaning provides cleaning services for Amber Inc., a business with four buildings. Crowne assigned different cleaning charges for each building based on the amount of square feet to be cleaned. The charges for the four buildings are $108,000, $102,600, $122,400, and $82,800. Amber secured this amount by signing a note bearing 8% interest on June 1. Required: Question Content Area 1. Prepare the journal entry to record the sale on June 1. If an amount box does not require an entry, leave it blank. 2. Determine how much interest Crowne will receive if the note is repaid on December 1. 3. prepare Crowne’s journal entry to record the cash received to pay off the note and interest on December 1. If an amount box does not require an entry, leave it blank. DO NOT GIVE SOLUTION IN IMAGEarrow_forward

- Revenue Journal The following revenue transactions occurred during November: Nov. 3. Issued Invoice No. 83 to Browning Company for services provided on account, $431. 12. Issued Invoice No. 84 to Triple A Inc. for services provided on account, $155. 28. Issued Invoice No. 85 to Whaley Co. for services provided on account, $596. Record these three transactions in the following revenue journal. REVENUE JOURNAL Accounts Rec. Dr. DATE Invoice No. Account Debited Post. Ref. Fees Earned Cr. Nov. 3 Nov. 12 Nov. 28arrow_forwardAdriana Graphic Design recelves $2,150 from a client billed in a previous month for services provided. Which of the following general journal entries will Adriana Graphic Design make to record this transaction? Multiple Choice 56:55 Cash 2,150 Accounts Receivable 2,150 Cash 2,150 Unearned Design Revenue 2,150 Accounts Receivable 2,150 Unearned Design Revenue 2,150 Accounts Payable 2,150 Design Revenue 2,150 MacBook Airarrow_forwardRevenue Journal The following revenue transactions occurred during November: Oct. 4. Issued Invoice No. 162 to Dawkins Co. for services provided on account, $320. Oct. 19. Issued Invoice No. 163 to City Electric Inc. for services provided on account, $245. Oct. 25. Issued Invoice No. 164 to Matthews Co. for services provided on account, $515. Record these three transactions into the following revenue journal.arrow_forward

- As part of the employment interview for an accounting job at Sound Design, you have been asked to answer the questions below, based on an invoice from one of Sound Design's vendors, Target Electronic Wholesalers. Invoice Table TARGET ELECTRONIC WHOLESALERS 1979 N.E. 123 Street Jacksonville, Florida 32204 Sold to: Sound Design 480 McDowell Rd. Phoenix, AZ 85008 Invoice Date: June 28, 20XX Terms of Sale: 3/15, n/30 ROG Stock # Description Unit Price Amount 4811V Stereo Receivers 50 x $292.50 = Blu-Ray Players Home Theater Systems 511CX 25 x $134.28 = 6146M 40 x $654.12 = 1031A LCD TVs 20 x $597.00% = Merchandise Total Insurance + Shipping $1,350.00 Invoice Total (a) Complete the invoice itemization by finding the total amount (in $) for each item, the merchandize total (in $), and the total amount of the invoice (in $). Stock # Description Unit Price Amount 4811V Stereo Receivers 50 x $292.50 $ 14,625 511CX Blu-Ray Players 25 x $134.28 $3,357 Home Theater Systems $ 26,165 6146M 40 x…arrow_forwardes The following transactions took place at the Cook Employment Agency during November 20X1. DATE TRANSACTIONS Nov. 5 Performed services for Job Search, Inc., for $31,000; received $14,500 in cash and the client promised to pay the balance in 60 days. 18 Purchased a graphing calculator for $380 and some supplies for $530 from Office Supply; issued Check 1008 for the total. 23 Received Invoice 1602 for $1,650 from Automotive Technicians Repair for repairs to the firm's automobile; issued Check 1009 for half the amount and arranged to pay the other half in 30 days. Prepare journal entries for the above transactions. View transaction list Journal entry worksheet < 1 2 Purchased a graphing calculator for $380 and some supplies for $530 from Office Supply; issued Check 1008 for the total. Date Nov 18, 20X1 3 Note: Enter debits before credits. Record entry General Journal Clear entry Debit Credit View general journalarrow_forwardAdriana Graphic Design receives $2,250 from a client billed in a previous month for services provided. Which of the following general journal entries will Adriana Graphic Design make to record this transaction? Multiple Choice Cash 2,250 Accounts Receivable 2,250 Cash 2,250 Unearned Design Revenue 2,250 Accounts Receivable 2,250 Unearned Design Revenue 2,250 Prev 3 of 10 Next > nere to search W P 99% 9:34 PM 2/21/2022arrow_forward

- As part of the employment interview for an accounting job at Sound Design, you have been asked to answer the questions below, based on an invoice from one of Sound Design's vendors, Target Electronic Wholesalers. Invoice Table TARGET ELECTRONIC WHOLESALERS 1979 N.E. 123 Street Jacksonville, Florida 32204 Sold to: Sound Design 480 McDowell Rd. Phoenix, AZ 85008 Invoice Date: June 28, 20XX Terms of Sale: 3/15, n/30 ROG Stock # Description Unit Price Amount 4811V Stereo Receivers 50 x $292.50 = 511CX Blu-Ray Players 25 x $134.28 = 6146M Home Theater Systems 40 x $654.12 = 1031A LCD TVs 20 x $597.00 = Merchandise Total Insurance + Shipping $1,350.00 Invoice Total (a) Complete the invoice itemization by finding the total amount (in $) for each item, the merchandize total (in $), and the total amount of the invoice (in $). Stock # Description Unit Price Amount 4811V Stereo Receivers 50 x $292.50 $ 511CX Blu-Ray Players 25 x $134.28 6146M Home Theater Systems 40 x $654.12 $ 1031A LCD TVs 20 x…arrow_forwardThe chart of accounts of the Barnes School is shown here, followed by the transactions that took place during October of this year. Assets Revenue 111 Cash 113 Accounts Receivable 115 Prepaid Insurance 124 Equipment 127 Furniture Liabilities 221 Accounts Payable Owner's Equity 311 R. Barnes, Capital 312 R. Barnes, Drawing Oct. 1 Bought liability insurance for one year, $1,850, Ck. No. 1527. 3 Received a bill for advertising from Business Summary, $415. 4 Paid the rent for the current month, $1,870, Ck. No. 1528. 7 Received a bill for equipment repair from Fix-It Service, $318, Inv. No. 436. 10 Received and deposited tuition from students, $6,375. 411 Tuition Income 11 Received and paid the telephone bill $312, Ck. No. 1529. 15 Bought desks and chairs from The Oak Center, $1,980, paying $980 in cash and placing the balance on account, Ck. No. 1530. 18 Paid on account to Business Summary, $415, Ck. No. 1531. 21 R. Barnes withdrew $1,000 for personal use, Ck. No. 1532. 24 Received a bill…arrow_forwardReview the following transactions and prepare any necessary journal entries for Lands Inc. A. On December 10, Lands Inc. contracts with a supplier to purchase 450 plants for its merchandise inventory, on credit, for $12.50 each. Credit terms are 4/15, n/30 from the invoice date of December 10. B. On December 28, Lands pays the amount due in cash to the supplier.arrow_forward

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:CengagePrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College

Century 21 Accounting Multicolumn JournalAccountingISBN:9781337679503Author:GilbertsonPublisher:CengagePrinciples of Accounting Volume 1AccountingISBN:9781947172685Author:OpenStaxPublisher:OpenStax College Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning

Financial AccountingAccountingISBN:9781337272124Author:Carl Warren, James M. Reeve, Jonathan DuchacPublisher:Cengage Learning Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning

Cornerstones of Financial AccountingAccountingISBN:9781337690881Author:Jay Rich, Jeff JonesPublisher:Cengage Learning College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning

College Accounting, Chapters 1-27 (New in Account...AccountingISBN:9781305666160Author:James A. Heintz, Robert W. ParryPublisher:Cengage Learning