[This question concerns long-run equilibrium so all variables in the questions are long-run.] Suppose Firm X has a cost function C(q) = q3 - 20q2 + 150q, from which we can derive its average cost function and marginal cost function as: AC(q) = q2 – 20q + 150, MC(q) = 3q2 – 40q +150. In each of the following 3 questions, you are given 2 statements—a price/quantity information and a market structure. In each question, determine and explain whether the 2 statements are consistent with each other. The long-runpriceis $73 and Firm X produces 11units. Firm X is in a perfectly competitive industry The long-run price is $73 and Firm X produces 11 units. Firm X is in a competitive selection industry. The long-run price is $75 and Firm X produces 5units. Firm X is in a monopolistically competitive industry.

-

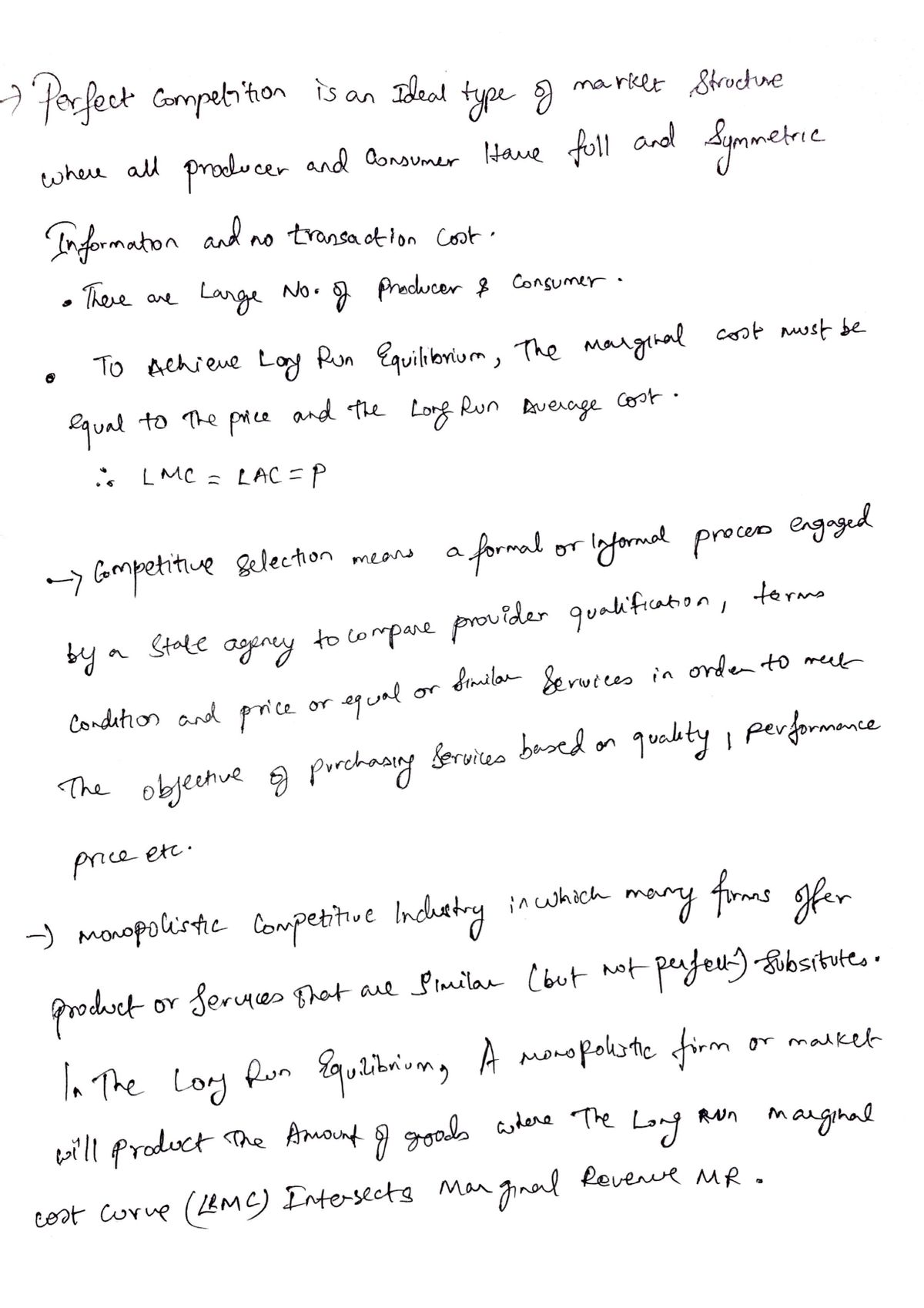

[This question concerns long-run equilibrium so all variables in the questions are long-run.]

Suppose Firm X has a cost functionC(q) = q3 - 20q2 + 150q,

from which we can derive its average cost function and marginal cost

function as:

AC(q) = q2 – 20q + 150, MC(q) = 3q2 – 40q +150.

In each of the following 3 questions, you are given 2 statements—a price/quantity information and a market structure. In each question, determine and explain whether the 2 statements are consistent with each other.

-

The long-runpriceis $73 and Firm X produces 11units. Firm X is in a

perfectly competitive industry -

The long-run price is $73 and Firm X produces 11 units. Firm X is in a competitive selection industry.

-

The long-run price is $75 and Firm X produces 5units. Firm X is in a

monopolistically competitive industry.

ANSWER

Trending now

This is a popular solution!

Step by step

Solved in 2 steps with 3 images